Inheritance Tax Australia technically does not exist. However, if you inherited a property and later want to sell it, you would need to pay capital gain tax australia. In this blog, we will cover:

- What is CGT Inheritance Tax Australia?

- How to calculate CGT Tax on inherited property Sale?

- Which Properties are exempt from CGT?

- How to work out if your property is eligible for CGT tax?

What is CGT Rule on On Inherited Property Sales Australia?

Capital Gains Tax (CGT) on the sale of inherited property in Australia is determined by several factors, including when the property was originally acquired by the deceased, its use, and the timing of the sale after inheritance. Here’s an overview of when and how much CGT may apply:

- Pre-CGT (before 20 September 1985): If the deceased acquired the property before this date, the property is generally exempt from CGT. However, if major improvements were made after this date, those improvements might be subject to CGT.

- Post-CGT (on or after 20 September 1985): If the property was acquired on or after this date, CGT is likely to apply on any capital gain realized from the sale.

How to Calculate CGT Inheritance Tax Australia?

The CGT is calculated based on the capital gain, which is the difference between the sale price and the cost base. For inherited properties, the cost base is usually the market value of the property at the time of the deceased’s death, plus any costs associated with acquiring, holding, and improving the property.

The actual amount of CGT depends on the individual’s marginal tax rate and the size of the capital gain. If the property has been held for more than 12 months, a 50% CGT discount may apply for individual taxpayers, effectively halving the taxable gain.

Let’s Take an Example:

Suppose you inherited a property valued at $500,000 at the time of the deceased’s death and later sold it for $700,000. The capital gain is $200,000. If you’re eligible for the 50% CGT discount, the taxable gain becomes $100,000. The tax on this amount would depend on your marginal tax rate.

Is Your Property Eligible for Inheritance Tax?

When dealing with the tax implications of selling inherited property in Australia, there are several key questions you should ask to understand how the tax might apply to your situation. Keep in mind that while there is no specific “inheritance tax” in Australia, capital gains tax (CGT) can apply to the sale of inherited property.

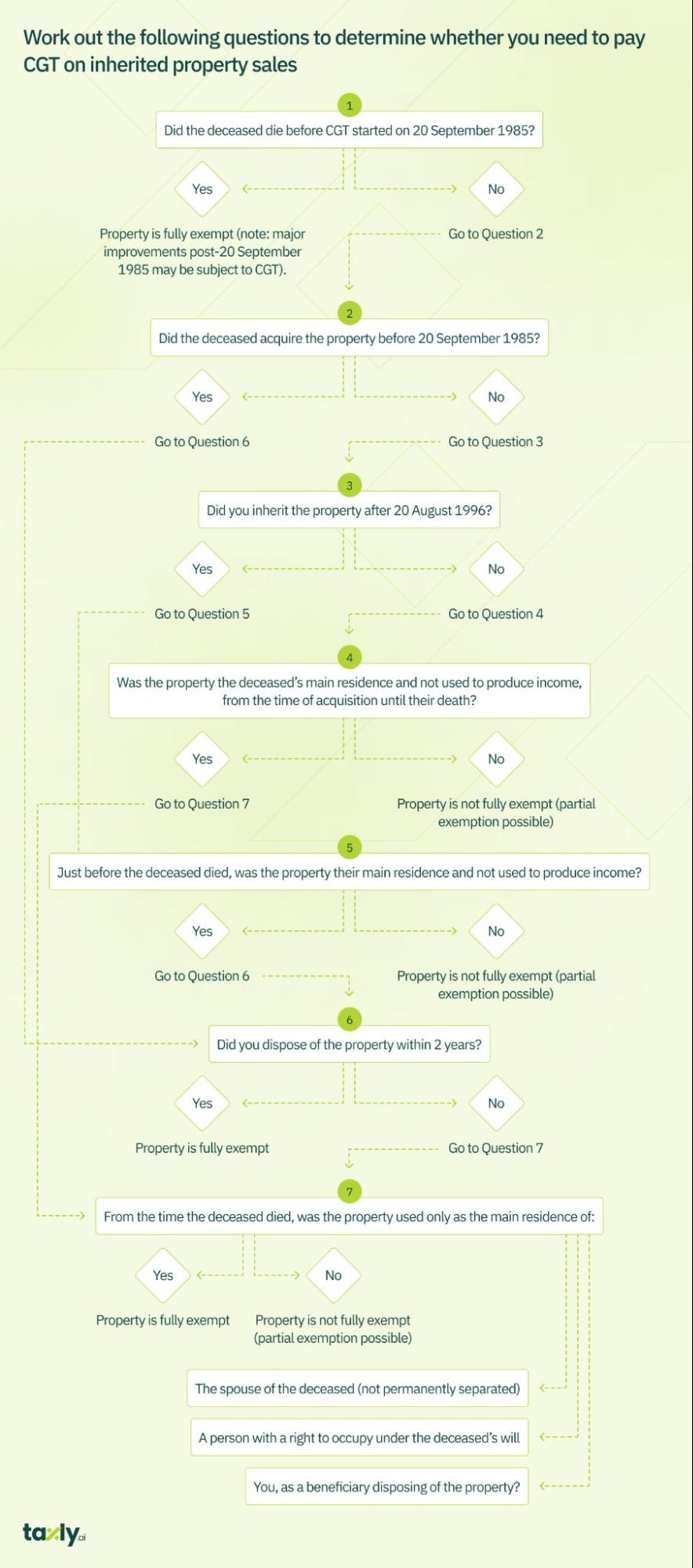

Work out the following questions to determine whether you need to pay CGT on inherited property sales:

1. Did the deceased die before CGT started on 20 September 1985?

– Yes: Property is fully exempt (note: major improvements post-20 September 1985 may be subject to CGT).

– No: Go to Question 2.

2. Did the deceased acquire the property before 20 September 1985?

– Yes: Go to Question 6.

– No: Go to Question 3.

3. Did you inherit the property after 20 August 1996?

– Yes: Go to Question 5.

– No: Go to Question 4.

4. Was the property the deceased’s main residence and not used to produce income, from the time of acquisition until their death?

– Yes: Go to Question 7.

– No: Property is not fully exempt (partial exemption possible).

5. Just before the deceased died, was the property their main residence and not used to produce income?

– Yes: Go to Question 6.

– No: Property is not fully exempt (partial exemption possible).

6. Did you dispose of the property within 2 years?

– Yes: Property is fully exempt.

– No: Go to Question 7.

7. From the time the deceased died, was the property used only as the main residence of:

– The spouse of the deceased (not permanently separated),

– A person with a right to occupy under the deceased’s will,

– You, as a beneficiary disposing of the property?

– Yes: Property is fully exempt.

– No: Property is not fully exempt (partial exemption possible).

Which Properties are Exempt from Inheritance Tax Australia?

In Australia, certain types of property sales are exempt from Capital Gains Tax (CGT). These exemptions are based on the nature of the property and its use. Here are some of the key categories of property sales that are typically exempt from CGT:

Main Residence Exemption:

The sale of a property that is your main residence (your home) is usually exempt from CGT. This exemption applies if the property has been your home for the entire period you owned it, has not been used to produce assessable income (like renting it out), and is on land of two hectares or less.

Criteria:

- The property must have been your home for the entire period you owned it.

- It should not have been used to produce assessable income, like renting it out.

- The land on which the home is situated is 2 hectares or less.

Temporary Absence Rule:

If you move out of your home and rent it out, the property can still be treated as your main residence for up to six years for CGT purposes, as long as you don’t treat another property as your main residence.

- You can treat the property as your main residence even if you are not living in it.

- The exemption can apply for a period of up to six years if the property is rented out (or indefinitely if not rented). Click here for our guide to investment property tax.

Disposal Within Two-Years Exemption:

If you inherit a property that was the main residence of the deceased and sell it within two years of the deceased’s death, it may be exempt from CGT.

- The property was the main residence of the deceased when they died, or they were not entitled to a main residence exemption on another property.

- The property is sold within two years of the deceased’s death.

Property Acquired Before CGT Commenced:

Properties acquired before the introduction of CGT on 20 September 1985 are generally exempt from CGT.

Small Business Concessions:

Certain small business assets may be exempt from CGT, particularly under the small business 15-year exemption, 50% active asset reduction, retirement exemption, and the rollover concession.

- The asset must be used in a small business or be an active asset of the business.

- Additional requirements include passing the “active asset test” and meeting specific turnover or net asset value thresholds.

Compulsory Acquisition:

CGT may not apply to a property that is compulsorily acquired by an Australian government agency.

Certain Other Exemptions:

Properties used to produce income for charities or religious institutions might also be exempt from CGT.

CGT Rules for Foreign Residents

The rules for foreign residents who inherit property can be quite different from those for Australian residents, particularly in relation to Capital Gains Tax (CGT). Here are the key aspects to consider:

CGT on Inherited Property:

As with Australian residents, foreign residents may also be subject to CGT on the sale of Australian property they have inherited. The CGT calculation is based on the increase in value of the property from the date the deceased acquired it to the date of sale, with some adjustments.

Main Residence Exemption:

Changes in Australian tax law have affected the availability of the main residence exemption for foreign residents. As of the last update in April 2023, foreign residents are generally not entitled to the main residence CGT exemption, with limited exceptions. This applies to properties sold on or after 30 June 2020.

One key exception is if the foreign resident, their spouse, or their minor children were temporary residents of Australia for some part of the period of ownership and the property was their main residence during that time.

Deceased Estates:

If the deceased was a foreign resident at the time of their death, the same CGT rules apply to the beneficiary, who may also be a foreign resident.

If the deceased was an Australian resident but the beneficiary is a foreign resident, the beneficiary will inherit the property with its market value as at the date of death as the cost base for future CGT calculations.

Six-Year Absence Rule:

The six-year absence rule allows a property to be treated as a main residence even if the owner is not living in it, under certain conditions. However, this rule might not apply to foreign residents in the same way it does for Australian residents, particularly if the property is rented out.

Tax Treaties and Double Taxation:

Depending on the country of residence of the foreign beneficiary, tax treaties between Australia and that country might affect how the inheritance is taxed. In some cases, this can prevent double taxation.

Reporting and Compliance:

Foreign residents are required to report any capital gain or loss from the sale of Australian property in an Australian tax return.

Withholding Tax:

In some situations, the buyer of the property may be required to withhold a percentage of the sale price and remit it to the Australian Taxation Office (ATO) as a precaution against unpaid CGT.

Suggested Read: What Does Tax Withheld Mean in Australia?

Final Word

If the property was the deceased’s main residence, acquired before 20 September 1985, or sold within two years of inheritance, it’s likely exempt from CGT. Otherwise, CGT is calculated on the difference between the property’s market value at the time of inheritance and its selling price.

Simplify Your CGT Inheritance Tax Calculations using Taxly.Ai

Our intuitive platform streamlines the process, ensuring accuracy and compliance with Australian tax laws. Say goodbye to complexity and hello to effortless CGT calculations. Try Taxly.ai and automatically detect your CGT exemptions today!

Discover More Topics

- What is a Tax Offset? [Explained With Example]

- Corporate Tax Australia – Complete Guide

- Maximize Your Deductions with Taxly.ai Tax Depreciation Schedule

Comments are closed