What is Tax Depreciation? Tax depreciation is a tax deduction that property investors can claim for the natural wear and tear of a property and its assets over time. It reflects the declining value of the property’s structure and the assets within it. In accounting, this is recognized as a decrease in the value of an asset over its useful life.

Why Claim Tax Depreciation?

- Reduce Taxable Income: Claiming tax depreciation lowers your taxable income. This can significantly reduce your tax bill, effectively putting more money back in your pocket each year.

- Improve Cash Flow: By reducing your tax liability, you effectively increase your annual cash flow. This can be particularly beneficial for property investors who rely on rental income.

- Maximize Investment Return: Depreciation is a non-cash deduction – it doesn’t come out of your pocket on an annual basis. Claiming it ensures you’re maximizing the return on your investment property.

- Property Value Appreciation: Even as your property appreciates in market value, you can still claim depreciation on the building and its fixtures and fittings, enhancing the investment’s profitability.

Who Can Claim Tax Depreciation?

- Individual Property Investors: Individuals who own investment properties, such as rental homes or commercial properties, are eligible to claim tax depreciation.

- Companies: Companies that own investment properties can claim depreciation on these assets. This includes properties used for business purposes or as rental investments.

- Trusts: Trusts, including discretionary trusts and family trusts that hold investment properties, can claim tax depreciation for those properties.

- Self-Managed Superannuation Funds (SMSFs): SMSFs that invest in property can claim tax depreciation on their investment properties, provided these investments comply with the superannuation laws.

- Partnerships: Business partnerships that own investment properties are eligible to claim tax depreciation, with the deductions distributed according to the partnership agreement.

- Joint Property Owners: Individuals who co-own an investment property can each claim their share of the property’s depreciation. The claim is typically proportional to the ownership interest.

- Property Developers: In some cases, property developers who hold onto some of the properties they develop as rental investments can claim tax depreciation.

- Overseas Property Investors: Non-resident investors who own taxable Australian property are also eligible to claim depreciation on these investments.

What to Claim?

In Australia, tax depreciable assets are items within an investment property that decrease in value over time due to wear and tear, aging, or obsolescence. These assets are categorized into two main types for tax depreciation purposes:

- Capital Works Deductions (Division 43):

This includes not just the building structure but also any structural improvements made over the years. Examples include:

- The construction cost of the building itself (walls, floors, roofing).

- Permanent structural improvements like renovations or extensions.

- Built-in kitchen cabinets, doors, windows, and sinks.

- Electrical wiring, plumbing, and gas systems.

Typically, the depreciation rate for capital works (the building’s structure and fixed items) is 2.5% per year. Capital works deductions are generally claimed over a 40 years property depreciation period. It is applicable for properties constructed after 15th September 1987.

- Plant and Equipment Deductions (Division 40):

It includes removable assets and fittings like garden machinery, exhaust fans, garage door motors, and even some types of light fixtures. Examples include:

- Appliances like ovens, dishwashers, and air conditioners.

- Carpets, blinds, and curtains.

- Furniture and freestanding cabinets.

- Security systems and smoke alarms.

The effective life and depreciation rate for each plant and equipment item are determined by the Australian Taxation Office (ATO). The depreciation rate for these items can be faster and varies based on the effective life of each asset.

Can You Claim Property Renovations?

Yes, you can. When you or a previous owner have renovated a property in Australia, you can claim depreciation on the costs associated with these renovations and improvements. Here’s a list of what can be claimed:

- Structural Improvements: Any structural changes or improvements made to the property, such as adding new rooms, extending the building, or making alterations to the floor plan.

- Roofing: The cost of replacing or repairing the roof of the property.

- Flooring: Expenses related to installing new flooring, such as carpets, tiles, or floorboards.

- Bathroom and Kitchen Renovations: The costs of renovating bathrooms and kitchens, including fixtures, fittings, and cabinetry.

- Plumbing and Electrical Work: Expenses for plumbing and electrical upgrades or repairs.

- Painting: Costs associated with interior and exterior painting of the property.

- Outdoor Improvements: Expenses for outdoor improvements, such as landscaping, fencing, or the construction of a new deck or patio.

- Extensions and Additions: Any additions or extensions to the property, such as adding a new bedroom, living area, or garage.

- Fixtures and Fittings: The cost of installing new fixtures and fittings, including lighting, built-in wardrobes, and security systems.

- Renewed or Repaired Appliances: Expenses for repairing or replacing appliances like air conditioning units, hot water systems, or ovens.

- Window Replacements: Costs associated with replacing windows or doors.

- Re-plastering or Rendering: Expenses for re-plastering or rendering internal or external walls.

It’s important to keep detailed records of all expenses related to these renovations and improvements, including invoices, receipts, and documentation of the work done. A Quantity Surveyor can help assess and quantify these costs accurately for inclusion in your tax depreciation schedule. This allows you to claim depreciation on these improvements over time, providing potential tax benefits for property investors.

Record Keeping for Depreciating Assets Claims

To claim tax depreciation in Australia, it’s essential to maintain detailed records of your property-related expenses and other relevant documentation. Here are the records you should keep:

- Purchase Documents:

- Contract of sale: The purchase contract for the property.

- Settlement statement: Records related to the property’s purchase, including stamp duty, legal fees, and settlement costs.

- Loan documents: If you used a loan to purchase the property, maintain records of the loan agreement and repayments.

- Property Cost and Acquisition Expenses:

Records of the property’s purchase price, including any additional costs like legal fees, title searches, and conveyancing fees.

- Depreciable Assets:

Invoices and receipts for the purchase of plant and equipment assets within the property, including appliances, fixtures, and fittings.

- Renovation and Improvement Expenses:

Invoices, receipts, and records of expenses related to property renovations and improvements, including structural changes, roofing, flooring, bathroom and kitchen renovations, plumbing, electrical work, painting, outdoor improvements, and extensions.

- Depreciation Schedule:

A copy of the tax depreciation schedule prepared by a qualified Quantity Surveyor. This schedule should detail all depreciable assets, their effective lives, and depreciation rates.

- Asset Register:

Maintain an asset register that lists all depreciable assets within the property. Include details like the asset’s description, date of purchase, cost, and any additional relevant information.

- Property Inspection and Valuation Reports:

If applicable, records of property inspections and valuation reports can be helpful for determining the property’s condition and value at various points in time.

- Apportionment Records:

If the property is used for both income-producing and private purposes (e.g., a home office), keep records of the apportionment calculations to claim deductions accurately.

Suggested Read: Work from Home Tax Deduction In Australia: Check Your Eligibility

- Ownership Records:

Records related to the ownership structure of the property, including trust deeds, company records, or SMSF documentation, if applicable.

- Relevant Correspondence:

Any correspondence with property managers, tenants, or contractors related to the property’s maintenance or improvements.

- Council Approvals and Permits:

Copies of council approvals and permits for renovations or extensions, if applicable.

- Bank Statements:

- Bank statements showing expenses related to the property, such as mortgage interest payments, property management fees, and insurance premiums.

- Tax Returns and Notices of Assessment:

Copies of your annual tax returns and notices of assessment, as these will reflect your claimed deductions.

- Correspondence with Tax Professionals:

Any correspondence or advice from tax professionals or accountants regarding your property’s tax depreciation claims.

- Lease Agreements:

If the property is rented out, maintain copies of lease agreements and rental income records.

By keeping these records organized and up-to-date, you can accurately claim tax depreciation deductions and ensure compliance with Australian tax laws. It’s advisable to consult with a tax professional or Quantity Surveyor to help you navigate the process and ensure that you’re maximizing your depreciation claims.

Tax Depreciation Rates for Investment Properties

In Australia, the tax depreciation rates for investment properties are determined by the Australian Taxation Office (ATO) and depend on the type of asset and the method of depreciation used. Here’s a general guide to understanding these rates:

- Capital Works Deductions (Division 43):

Typically, the depreciation rate for capital works (the building’s structure and fixed items) is 2.5% per year.

This rate applies to residential properties built after 15th September 1987.

The depreciation is claimable over 40 years.

- Plant and Equipment Deductions (Division 40):

The depreciation rates for plant and equipment (removable fixtures and fittings) vary based on the effective life of each asset, as determined by the ATO.

The ATO provides a detailed list of assets and their effective lives, which can be used to calculate the depreciation rate.

For example, if an asset has an effective life of 10 years, the diminishing value rate would be 20% (using the 200% diminishing value method), and the prime cost rate would be 10%.

Low-Value Pooling:

Certain low-cost and low-value assets can be pooled to simplify depreciation calculations and potentially accelerate deductions.

Low-cost assets (costing less than $1,000) and low-value assets (with a written-down value less than $1,000) can be placed in a low-value pool.

The depreciation rate for a low-value pool is 18.75% in the first year and 37.5% in subsequent years.

Immediate Write-Offs:

Some assets costing less than a certain threshold (which can change based on tax year and legislation) may be eligible for immediate write-off.

Software and Intangible Assets:

Depreciation rates for software and other intangible assets can also vary and are subject to specific ATO rules.

Two Methods to Calculate Tax Depreciation:

- Prime Cost Method (Straight Line Method):

This method spreads the deductions evenly over the effective life of the asset. The rate is 100% divided by the effective life.

This method provides a constant deduction rate for the entire effective life of the asset.

Depreciation is calculated as a fixed percentage of the asset’s cost.

The annual depreciation amount remains the same each year, offering a consistent tax deduction over the life of the asset.

Formula: Annual Depreciation = (Cost of Asset × (100% / Effective Life))

The Prime Cost method spreads out the benefits more evenly over time, which might be preferable for investors seeking consistent tax relief.

- Diminishing Value Method:

This method results in higher deductions in the early years of an asset’s life. The rate is calculated as 200% divided by the effective life of the asset.

Depreciation is calculated as a percentage of the remaining book value of the asset each year.

As a result, the depreciation amount decreases each year.

Formula: Annual Depreciation = (Remaining Book Value of Asset × (200% / Effective Life))

The Diminishing Value method front-loads the benefits, offering larger deductions in the early years. This might be attractive for investors wanting to maximize their short-term cash flow.

Who is Eligible?

To check your eligibility to claim tax depreciation on a property in Australia, you need to consider several key factors:

- Type of Property:

Generally, tax depreciation is available for investment properties. This includes both residential and commercial properties. Your own home, or principal place of residence, is not eligible for tax depreciation deductions.

- Date of Construction:

The construction date of your property affects your eligibility for capital works deductions (Division 43). For properties built after 15th September 1987, you can generally claim these deductions. The rate and period of depreciation can vary based on the exact construction date.

- Purchased New or Second-Hand:

Recent changes to the Australian tax law (as of 2017) affect the ability to claim depreciation on plant and equipment (Division 40) for second-hand residential properties. If you purchased a second-hand residential property after 9th May 2017, you might not be eligible to claim depreciation on existing plant and equipment. However, if you add new plant and equipment to the property, you can claim depreciation on these new assets.

- Renovations and Improvements:

If you or a previous owner have made renovations or improvements to the property, you may be able to claim depreciation on these costs, regardless of the property’s age. This includes both structural improvements (capital works) and new plant and equipment items.

- Commercial Properties and Other Special Cases:

Different rules can apply for commercial properties, properties used for both private and income-producing purposes, and properties owned by a trust or company.

- Ownership Structure:

The way your investment property is owned (individual, joint, company, trust, self-managed super fund, etc.) can also influence your eligibility for depreciation deductions.

To accurately determine your eligibility and ensure compliance with current tax laws, it’s advisable to:

- Consult a Tax Professional: An accountant or tax advisor, especially one experienced in property investment, can provide personalized advice based on your specific circumstances and the latest tax regulations.

- Obtain a Depreciation Schedule: A Quantity Surveyor specialized in tax depreciation can prepare a depreciation schedule for your property. This schedule will outline all the depreciation deductions you’re entitled to claim and is tailored to your property’s specifics, including its age, type, and any renovations or improvements made.

Remember, tax laws and regulations can change, so it’s important to seek up-to-date advice and ensure that your information is current.

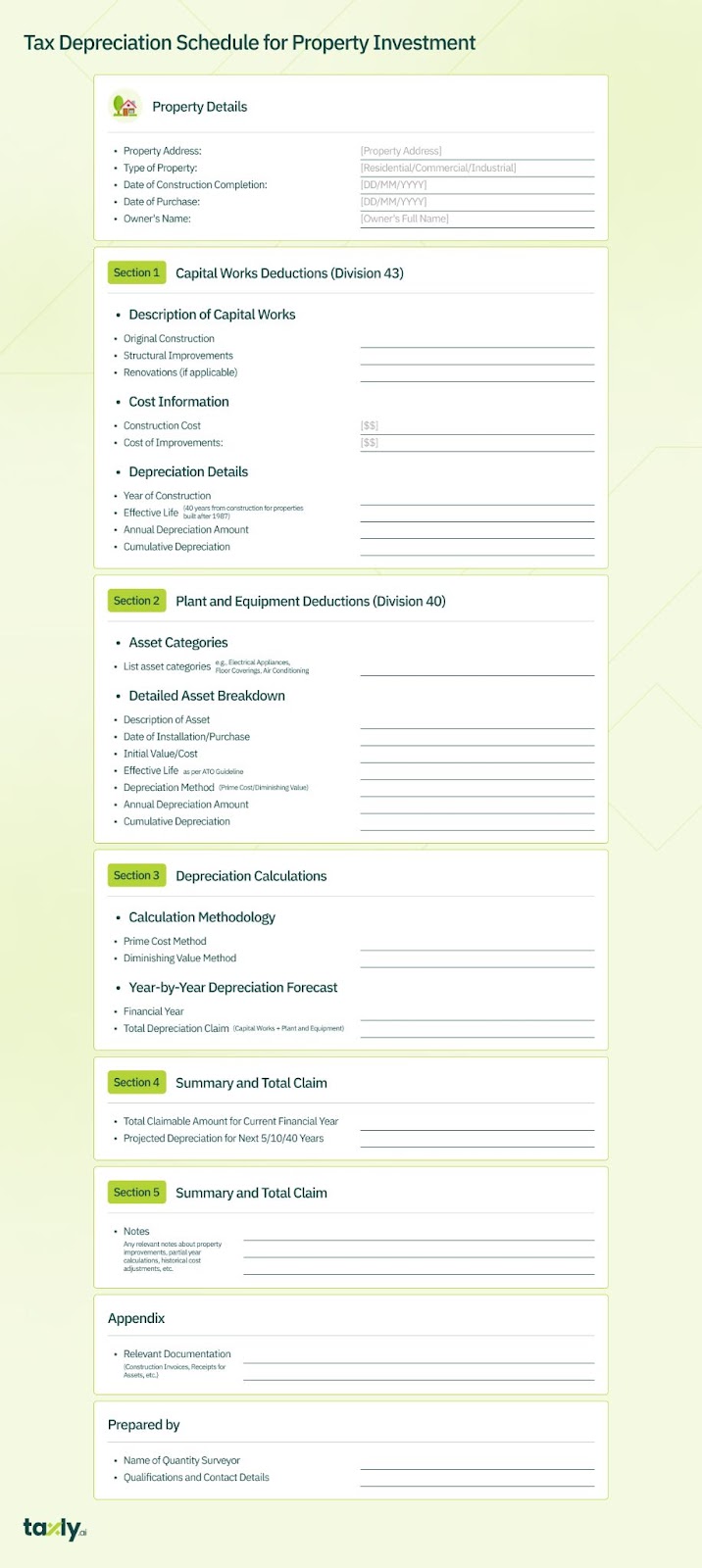

What to Include in a Tax Depreciation Schedule?

Check out our free Depreciation Schedule Template

Tax Depreciation Vs Franking Credits for Companies

How to Claim Depreciating Assets in Australia – Step by Step Process

Claiming tax depreciation in Australia involves a step-by-step process that ensures you accurately calculate and legitimately claim your deductions. Here’s a general guide to the process:

- Confirm Eligibility: Determine if your property is eligible for tax depreciation. This is typically applicable for investment properties, both residential and commercial. Check if your property meets the criteria for capital works deductions and plant and equipment depreciation.

- Understand Depreciable Assets: Familiarize yourself with the types of assets that can be depreciated in your property. This includes the building’s structure (capital works) and the fixtures and fittings (plant and equipment).

- Engage a Quantity Surveyor: Hire a qualified Quantity Surveyor who specializes in tax depreciation to prepare a tax depreciation schedule for your property. They are professionals authorized to assess construction costs for depreciation purposes when the original costs are unknown.

- Depreciation Schedule Preparation: The Quantity Surveyor will inspect your property and identify all depreciable assets. They will then prepare a comprehensive depreciation schedule that outlines the deductions you can claim over the life of the property.

- Record Keeping: Ensure you keep detailed records, including the date of purchase, cost of the property, and any subsequent expenditures on renovations or improvements. These records are vital for accurate depreciation calculations.

- Consult Your Accountant: Provide your tax accountant with the depreciation schedule. Your accountant will use this schedule to claim the appropriate depreciation deductions on your annual tax return.

- File Your Tax Return: Claim your depreciation deductions in your tax return. Ensure that all claims are accurate and in line with the depreciation schedule and ATO guidelines.

- Review Annually: Tax depreciation is an ongoing process. Review your property’s situation each year to account for any changes, such as additional renovations, changes in tax laws, or alterations to the property’s use.

- Stay Informed About Changes in Tax Laws: Tax laws and regulations can change, potentially affecting your eligibility and claims. Stay informed about any changes that might impact your investment property.

- Seek Professional Advice When Needed: If you have any doubts or specific questions about your situation, it’s wise to consult with tax professionals or financial advisors who specialize in property investment.

Auto-Scan and Claim Your Tax Depreciation Easily using Taxly.Ai

Claim your tax depreciation with ease and confidence using Taxly.Ai. Our AI Powered tax assistant app simplifies the claim process, helping you maximize your deductions effortlessly. Don’t miss out on valuable tax benefits – get started with Taxly.Ai today!

The Bottomline

Tax depreciation is a valuable tax deduction for property investors, as it reduces taxable income and improves cash flow. It’s applicable to various entities owning income-producing properties, and it encompasses claiming on both the property’s structure and its fixtures and equipment. To ensure accuracy and compliance with Australian Taxation Office (ATO) guidelines, it’s advisable to get a depreciation schedule prepared by a qualified Quantity Surveyor and to consult with a tax professional.

Comments are closed