Corporate tax in Australia is a levy imposed on the income of companies operating within the country. Here are key aspects of corporate tax in Australia:

Corporate Tax Australia Key Takeaways:

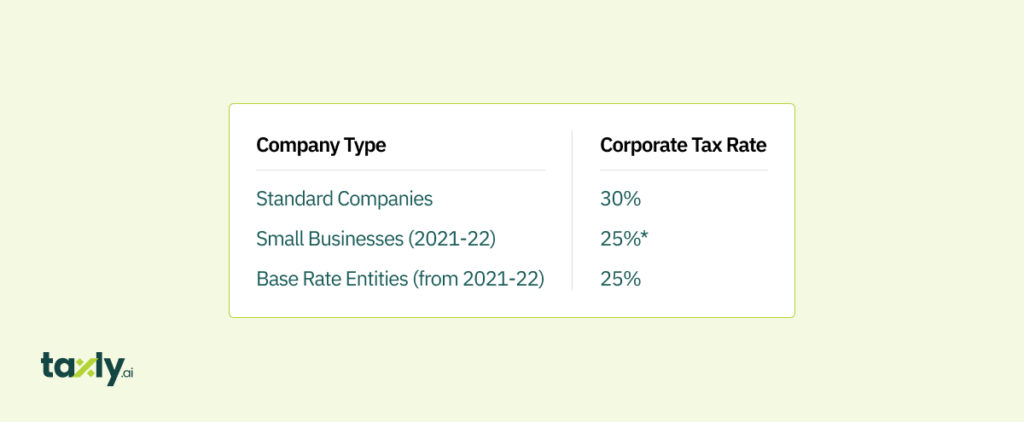

- The baseline corporate tax rate for the majority of companies is 30%.

- Small businesses enjoy a reduced tax rate of 25% if their aggregated turnover is below $50 million.

- The standard tax year in Australia spans from July to June, and companies can apply for alternative income years under specific conditions.

- Base rate entities must apply a reduced company tax rate of 25% starting from the 2021–22 income year.

- Corporate tax applies to a company’s taxable income, covering various sources such as business activities and capital gains.

- Companies can reduce their taxable income by claiming deductions for eligible business expenses and taking advantage of tax offsets.

- In addition to corporate income tax, businesses must navigate the Goods and Services Tax (GST) landscape in Australia.

- Businesses need to consider multiple taxes, including Capital Gains Tax and Goods and Services Tax, alongside corporate income tax.

*Note: The reduced tax rate for small businesses applies if the aggregated turnover is below $50 million in the 2021-22 income year.

Suggested Read: Sole Trader Tax Deductions in Australia: A Comprehensive Guide

Things to Know About Corporate Tax Australia

Standard Corporate Tax Rate:

The standard corporate tax rate in Australia is 30%. This rate applies to most companies operating in the country.

Example: ABC Pty Ltd, a manufacturing company, is subject to the standard corporate tax rate of 30% on its annual profits.

Lower Rates for Small Businesses:

Eligible small businesses, typically those with an annual turnover below a specified threshold, may benefit from a lower corporate tax rate. This reduced rate is commonly set at 27.5%, but the exact thresholds and rates can vary.

Example: XYZ Pty Ltd, a small software development startup with an annual turnover below the threshold, qualifies for the lower corporate tax rate of 27.5%.

Base Rate Entities:

Base rate entities may qualify for a lower tax rate. The definition of a base rate entity and the associated rates can change, so it’s crucial for companies to regularly check the ATO guidelines for updates.

Example: LMN Corporation, meeting the criteria as a base rate entity in the current financial year, enjoys a reduced corporate tax rate.

Franking Credits:

Companies in Australia may issue franking credits to shareholders. These credits allow shareholders to claim tax credits for the tax the company has already paid on its profits, preventing double taxation.

Example: Shareholders of DEF Ltd receive franking credits alongside dividends, allowing them to offset their personal income tax liabilities.

Carry-Forward of Losses:

Companies are permitted to carry forward tax losses to offset against future profits. This provision helps businesses recover from periods of financial difficulty.

Example: GHI Industries, which incurred losses in the previous financial year, carries forward those losses to reduce its taxable income in the current year.

Research and Development (R&D) Incentives:

Companies engaged in eligible R&D activities may be eligible for tax incentives. These incentives aim to encourage innovation and investment in research and development.

Example: MNO Innovations, a company heavily involved in R&D, benefits from tax incentives to support its groundbreaking projects.

Thin Capitalization Rules:

Australia has thin capitalization rules to limit the amount of debt a company can have in relation to its equity. This prevents excessive interest deductions.

Example: PQR Ltd ensures compliance with thin capitalization rules to maintain a balanced debt-to-equity ratio and optimize its tax position.

Transfer Pricing Rules:

Companies engaging in transactions with related parties must adhere to transfer pricing rules to ensure that these transactions are conducted at arm’s length, preventing potential tax avoidance.

Example: STU Corporation, with subsidiaries overseas, follows transfer pricing rules to establish fair values for transactions and comply with tax regulations.

Goods and Services Tax (GST):

Companies in Australia must comply with GST rules for the sale of goods and services, collecting and remitting GST as required by law.

Example: VWX Retailers include GST in the prices of its products and services, ensuring compliance with the GST regulations.

International Tax Agreements:

Australia has agreements with various countries to avoid double taxation and facilitate the exchange of tax information. These agreements provide clarity on tax liabilities for multinational companies operating across borders.

Example: ABC Global, an Australian company with international operations, benefits from tax agreements that prevent double taxation on its foreign income.

Compliance and Reporting:

Companies are obligated to comply with ATO reporting requirements, including the timely lodgment of annual tax returns.

Example: XYZ Enterprises ensures accurate and timely reporting, submitting its annual tax return to the ATO in accordance with compliance obligations.

Are There Any Corporate Tax Deductions Australia?

Australian Corporations are eligible for a range of corporate tax deductions, such as:

Operating Expenses:

Corporations can claim deductions for operating expenses incurred during the financial year. This includes costs such as office stationery, utility bills, and employee wages. These deductions are applicable in the year the expenses are incurred.

Example: ABC Enterprises, a manufacturing company, deducts the cost of raw materials, employee wages, and office supplies as operating expenses, thereby reducing its taxable income.

Suggested Read: What Can Hospitality Workers Claim on Tax – It’s Time to Treat YOU!

Accelerated Deductions:

Accelerated deductions are a mechanism that allows corporations to write off eligible assets faster than the standard depreciation schedule. This can include investments in technology or machinery.

Example: XYZ Tech Solutions purchases new computer servers for its operations. With accelerated deductions, the company can claim a faster write-off for these assets, reducing its taxable income.

Motor Vehicle Expenses:

Corporations can claim deductions for motor vehicle expenses incurred for business purposes. This includes fuel, maintenance, and depreciation of vehicles used in the course of business.

Example: LMN Logistics, a transportation company, claims deductions for fuel and maintenance costs associated with its delivery vehicles, reducing its overall taxable income.

Home-Based Business Expenses:

For corporations operating from home, deductions can be claimed for related expenses such as utilities, rent, and maintenance. This is applicable when part of the home is used exclusively for business purposes.

Example: DEF Consulting operates from a home office, allowing them to claim a portion of their rent and utility expenses as deductions, reducing their taxable income.

Suggested Read: Sole Trader Tax Deductions in Australia: A Comprehensive Guide

Business Travel Expenses:

Corporations can claim deductions for expenses related to business travel, including accommodation, meals, and transportation. This is applicable when employees travel for work-related purposes.

Example: GHI International sends its sales team to attend a trade show. The expenses for flights, accommodation, and meals incurred during the business trip are claimed as deductions.

Suggested Read: Your Complete Guide to Work Related Business Trip Tax Deduction

Workers’ Salaries, Wages, and Superannuation:

Deductions can be claimed for salaries, wages, and superannuation contributions made to employees. This includes regular payments and contributions to employee retirement savings.

Example: MNO Corporation deducts salaries and superannuation contributions made to its employees, reducing its taxable income while fulfilling its obligations to its workforce.

Research and Development (R&D) Tax Incentives:

Companies engaging in eligible R&D activities may benefit from tax incentives, providing a deduction for costs associated with research and development initiatives.

Example: PQR Innovations, involved in cutting-edge research, leverages R&D tax incentives to offset costs related to developing new technologies and products.

Other Industry-Related Deductions:

Certain industries may have specific deductions tailored to their nature of operations. These deductions could include specialized equipment, training costs, or compliance-related expenses.

Example: STU Pharmaceuticals claims deductions for expenses related to compliance with stringent regulations in the pharmaceutical industry, ensuring adherence to quality standards.

The Bottomline

Corporate tax in Australia is a 30% levy on companies’ income. Small businesses with a turnover below $50 million enjoy a reduced rate of 25%. The tax year runs from July to June, and companies can apply for alternative income years.

Corporate tax applies to taxable income, covering business activities, capital gains, and assessable income. Deductions, offsets, and compliance with Goods and Services Tax (GST) are integral. Additionally, businesses face Capital Gains Tax (CGT) alongside corporate income tax.

Explore More Topics

- What Does Tax Withheld Mean in Australia?

- Self Employed Vs Freelance Tax – Key Things to Know

- 10 Self-Employment Tax Deductions and Benefits for Australians

Comments are closed