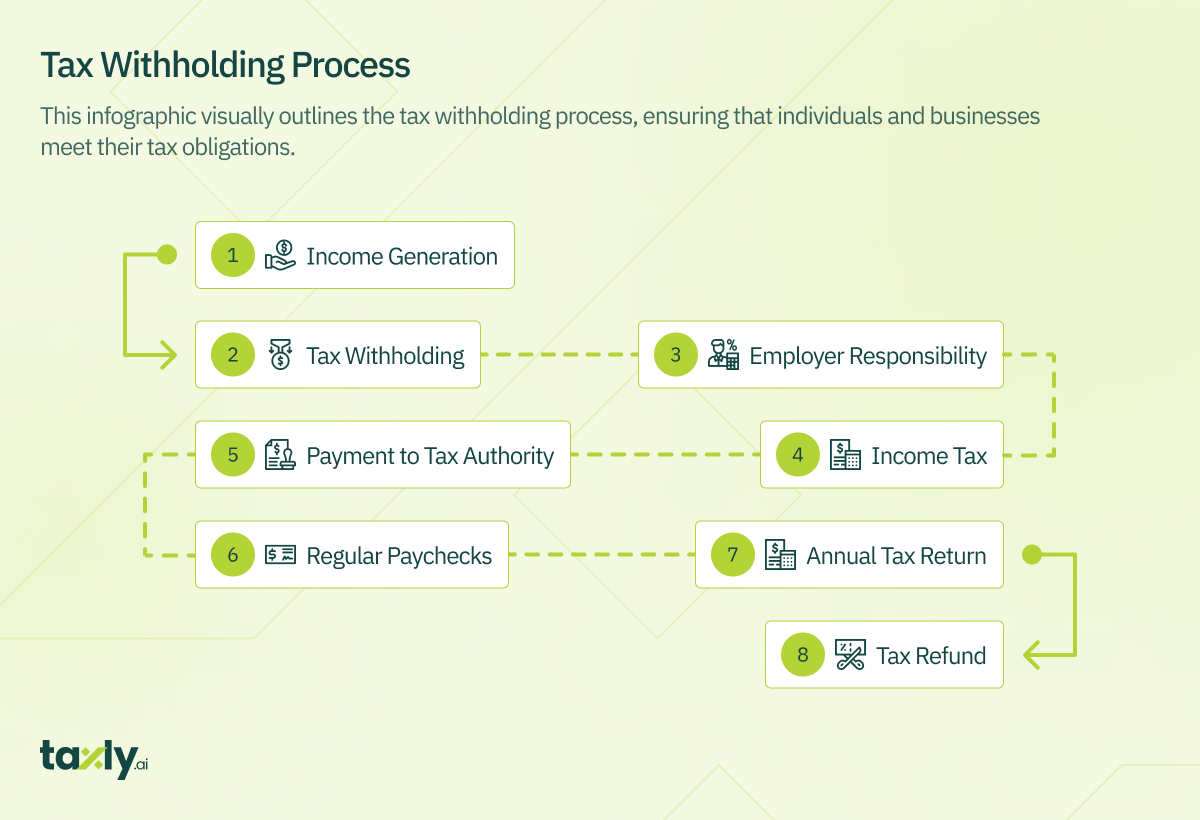

In Australia, “tax withheld” means the income tax deducted from employee’s wages or payments. It remits directly to the Australian Taxation Office (ATO) on the employee’s behalf.

Tax Withheld ensures year-round income tax payments, rather than significant tax billing at the financial year.

Tax withheld is a crucial part of the Australian taxation system. It affects a wide range of workers, including employees, contractors, and other businesses.

Tax is Withheld from Employee Payroll

When an employer pays an employee, they are required to withhold a portion of the employee’s gross wages as income tax before issuing the net pay. This withheld amount is then sent to the ATO.

Example: If an employee earns $50,000 per year, their employer will calculate and withhold a portion of this income for tax purposes, say $10,000. The employee will receive the remaining $40,000 as their net pay. The $10,000 withheld goes directly to the ATO.

Suggested Read: How to Avoid Contribution Tax – ATO Tax Threshold [Updated 2023-24]

Year-Round Income Tax Collection

The purpose of tax withholding is to prevent individuals from facing a substantial tax bill at the end of the financial year. By spreading the tax payment over each paycheck, it helps taxpayers budget and ensures the government receives its revenue regularly.

Tax Regulatory Compliance

Employers play a crucial role in ensuring tax compliance. They must accurately calculate and withhold the correct amount of tax based on the employee’s income, tax brackets, and any tax offsets or deductions they are entitled to.

Tax Withheld Reporting

Employers provide employees with payment summaries that detail the total income earned and the amount of tax withheld throughout the year. Employees use this information to complete their tax returns.

Tax Withheld Applies to Following Payment Types

- Employee Salaries

- Worker wages

- Director fees

- Payments to contractors who don’t quote their Australian Business Number (ABN).

How to Calculate Tax Withheld

The ATO provides online calculators to help employers and individuals determine the correct amount of tax to withhold. These tools take into account individual circumstances, such as deductions and tax offsets.

If you want to simplify the process of tax withheld calculation, try our AI powered tax automation app for Australians.

Tax Withheld and PAYG

Employers have specific obligations related to tax withholding, including registering for PAYG (Pay As You Go) withholding, paying withheld amounts to the ATO, reporting withheld amounts on activity statements, providing payment summaries to employees, and lodging an annual PAYG withholding report.

PAYG Record Keeping

Employers are required to maintain records related to PAYG withholding transactions for at least five years to ensure compliance with tax regulations.

You Must Withhold Tax To

- Ensure Regular Tax Payments

- Promote Tax Compliance

- Support Government Revenue

- Simplify Tax Filing

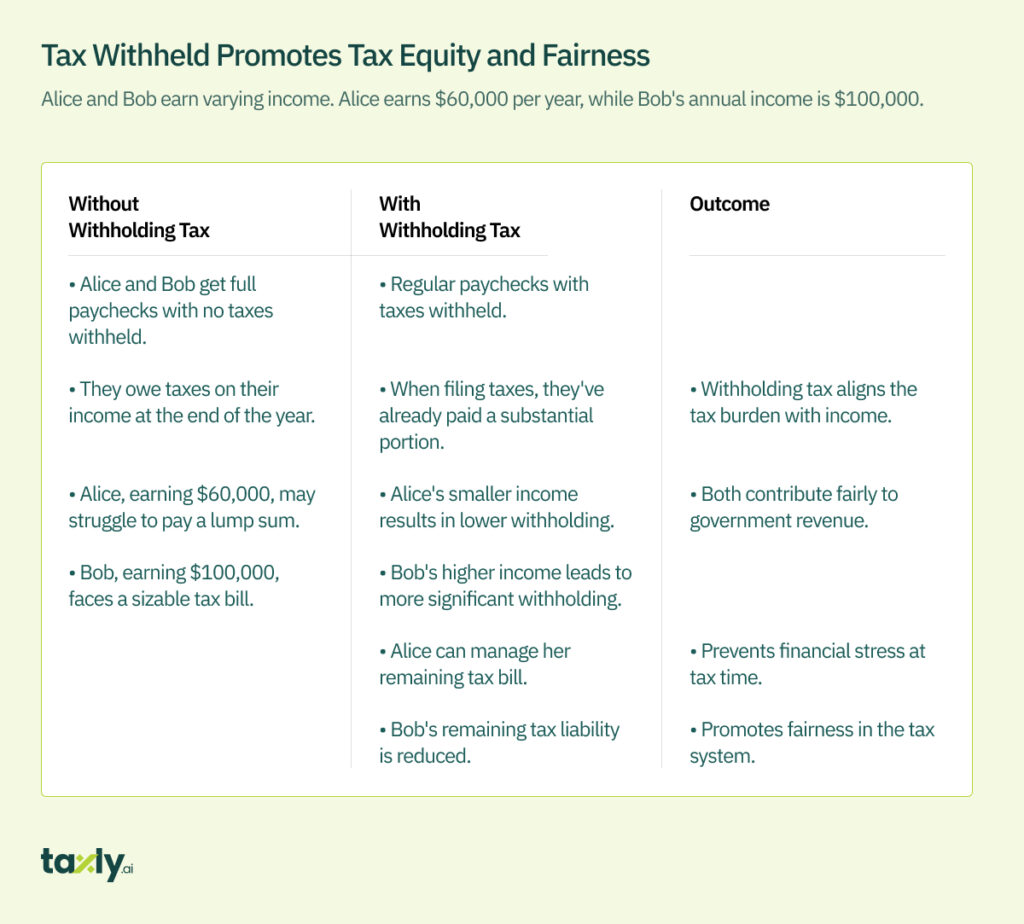

- Ensure Equity

- Align with Tax Law Changes

- Reduce Financial Burden

- Facilitate Government Budgeting

- Minimize Collection Costs

- Prevent Tax Refund Delays

3 Types of Tax Withholders in Australia

1. Small Withholders

- Withholds $25,000 or less in income tax each year.

- Pays withholding amounts to the Australian Taxation Office (ATO) every quarter.

- Reports withholding on activity statements received each quarter.

- Can arrange to receive monthly activity statements by contacting the ATO’s extended-hours business service.

Example: A small business that withholds $20,000 in income tax from its employees’ wages each year is considered a small withholder.

2. Medium Withholders

- Withholds income tax ranging from $25,001 to $1 million annually.

- Pays withholding amounts to the ATO every month.

- Reports withholding on activity statements received each month.

Fact: Medium withholders handle a moderate amount of income tax withholding compared to small withholders.

3. Large Withholders

- An individual or business that withheld amounts totaling more than $1 million in income tax in a previous financial year or is part of a company group that has withheld more than $1 million in a previous financial year.

- Amounts withheld are paid and sent electronically to the ATO twice a week.

- Payment due dates depend on the day withholding took place.

Example: A major corporation that withholds millions of dollars in income tax from its employees and contractors is classified as a large withholder.

Payment Due Dates for Large Withholders

- If withholding occurs on Monday or Tuesday, payment is due the following Monday.

- If withholding occurs on Wednesday, payment is due on the second Thursday after that day.

- If withholding occurs on Thursday or Friday, payment is due the following Thursday.

- If withholding occurs on Saturday or Sunday, payment is due on the second Monday after that day.

Payment due dates are adjusted for public holidays, allowing for payments on the next working day when the due date falls on a holiday.

Large Withholder’s Discretionary Extensions to Payments

- Large withholders may occasionally make payments of small amounts outside their regular payment cycle.

- They can delay payment to the ATO until the next regular payment date if the amount is either 0.5% of the amount withheld in the previous financial year or $50,000, whichever is less.

- Requests for extensions beyond this threshold must be made in writing to the Commissioner, stating the reasons for the extension.

- Such extensions are granted only in rare circumstances and are assessed on a case-by-case basis.

When is Tax Withheld Applicable?

Tax withholding occurs in various situations and applies to payments made to different categories of individuals or entities. Here’s a clear breakdown of when tax withholding takes place and from which payments:

1. Employee Wages:

Employers withhold tax from the wages of their employees.

This includes salaries, hourly wages, bonuses, and commissions.

Example: An employee earning $60,000 per year has tax withheld from each paycheck.

2. Independent Contractors:

Businesses withhold tax from payments made to independent contractors who don’t provide an Australian Business Number (ABN).

These contractors are subject to PAYG withholding.

Example: A business pays a contractor $5,000 for services, with tax withheld if the contractor doesn’t quote an ABN.

3. Directors’ Fees:

Directors’ fees paid to company directors are subject to tax withholding.

Example: A company pays directors’ fees to its board members, with tax withheld from these payments.

4. Voluntary Agreements:

Payments made under voluntary agreements, such as those to subcontractors, may be subject to withholding tax.

Example: A business has a voluntary agreement with a subcontractor and withholds tax from their payments.

5. Payments to Businesses without ABNs:

Payments made to businesses or contractors that fail to provide an ABN may be subject to withholding tax.

Example:

A business pays a cleaning company for services, and tax is withheld because the cleaning company didn’t provide an ABN.

6. Nonresident Aliens:

Nonresident aliens who earn income from Australian sources, such as interest, dividends, or wages, may have tax withheld.

Example:

An international student working in Australia has tax withheld from their wages.

7. Interest and Dividends:

Individuals and entities may have tax withheld from interest and dividend payments from Australian sources.

Example:

An individual receives dividends from shares in an Australian company, and tax is withheld on these dividends.

8. Special Payments:

Some payments, such as those made to seasonal workers, nannies, and cleaners, may have specific tax withholding rules.

Example:

A farmer pays seasonal workers, with tax withheld as per special withholding rules.

9. Tax on Pensions:

Tax may be withheld from pension payments, such as superannuation income stream payments.

Example:

A retiree receives a superannuation income stream, and tax is withheld from these payments.

10. Large Transactions:

In certain circumstances, tax may be withheld from large transactions, like the sale of property by foreign residents.

For Example:

A foreign resident sells an Australian property, and tax is withheld on the sale proceeds.

11. Termination Payments:

When employees leave a job, their final payments may be tax withheld.

12. Personal Services Income (PSI):

Tax withholding can apply to payments related to Personal Services Income (PSI) under certain conditions.

For example:

A consultant provides services, and tax is withheld as PSI rules apply.

** Sole Traders and Partnerships Are Exempt

Sole traders and partnerships are exempt from withholding tax on amounts taken from the business for personal use, but they must include this income in their tax return.

Suggested Read: Australian Goods and Service Tax [EXPLAINED]

What Happens When Employees Retire or Leave?

When employees leave or retire in Australia, several important steps and obligations come into play. Here’s a clear breakdown of what happens when employees leave or retire:

1. Final PAYG Withholding Payments:

Employers must make final PAYG withholding payments on behalf of departing employees.

This includes withholding tax from any final payments made to the employee, such as salary, accrued leave, or termination payments.

2. PAYG Payment Summary – Employment Termination Payment (ETP):

Employers are required to complete a PAYG Payment Summary – Employment Termination Payment (ETP) for departing employees.

This summary details the final payments, including any amounts withheld for tax purposes.

The PAYG Payment Summary – ETP is typically provided to the employee by July 14th following the financial year in which the termination occurred.

3. Send PAYG Summaries to Employees:

Employers must send the PAYG Payment Summary – ETP to the departing employee by the specified deadline.

This summary outlines how much the employee was paid during the financial year and how much tax was withheld.

Electronic payment summaries can be provided to employees as long as they meet formatting requirements when lodged online.

4. TFN Declaration:

Employers must retain the departing employee’s Tax File Number (TFN) declaration until the end of the next financial year.

This is important for record-keeping and potential audits.

5. Check Final Details:

Employers include the details of any final payments made to the departing employee in the PAYG Payment Summary Statement.

The PAYG Payment Summary Statement is an annual report that provides a summary of all PAYG withholding activities for the financial year.

6. Superannuation and FBT Obligations:

Employers may have superannuation and fringe benefit tax (FBT) obligations when employees leave.

These obligations should be addressed in compliance with relevant regulations.

7. Termination Record-Keeping:

Employers are required to keep records related to employment termination payments for at least five years.

8. Other Considerations:

Employers and employees should also consider factors such as any outstanding leave balances, notice periods, and post-employment benefits when an employee leaves or retires.

When Are You No Longer Required to Withhold Tax?

You are no longer required to withhold tax in Australia under specific circumstances. Here’s a clear breakdown of when you are no longer required to withhold tax:

- Ceasing to Have Employees:

If your business no longer has employees, you can cancel your registration for PAYG withholding.

Example: A small business owner who had employees decides to close the business, and therefore, there are no more employees to withhold tax from.

- Meeting All Tax Obligations:

Before canceling your PAYG withholding registration, you must ensure that you have met all your PAYG withholding obligations.

This includes paying all withheld amounts to the Australian Taxation Office (ATO) and lodging all outstanding activity statements and annual reports.

Suggested Read: Tax Penalties Australia – Can ATO Send You to Jail?

Is Tax Withheld Deductible?

Tax withheld represents the money that your employer or payer deducts from your income and sends directly to the Australian Taxation Office (ATO) on your behalf. It’s essentially a prepayment of your income tax based on your earnings.

Because tax withheld is already a payment toward your income tax obligation, it cannot be deducted again as an expense when determining your taxable income. In simpler terms, you cannot claim a deduction for the tax that has already been withheld from your income.

However, it’s important to note that there are other types of deductions and tax offsets available that can potentially reduce your taxable income. These include expenses related to your work, self-education, medical costs, and more. These deductions and offsets are separate from the tax withheld from your income.

To make the most of available deductions and offsets, maintain accurate records of your income, expenses, and deductions.

Automate your potential tax deductions using an AI powered tax deductions app.

You can also seek guidance from a tax professional or refer to the Australian Taxation Office’s guidelines when preparing your annual tax return.

The Bottomline

Tax withheld is an important part of the Australian taxation system which saves employers from huge tax burdens at the end of the financial year. It not only keeps the money circulating in the tax system and Australian economy but also offers significant financial record keeping relief to employers.

Here are a few more suggested reads from our blog,

- How to Do Tax Accounting in Australia – Beginner’s Guide

- What is Death Tax Australia? [Complete Guide]

- Self Employed Vs Freelance Tax – Key Things to Know

- Australian Goods and Service Tax [EXPLAINED]

Comments are closed