If you want to sell investment property in Australia, you will need to pay Capital Gains Tax. CGT is an integral aspect of investment planning, and knowing how it works can help you reduce its implications. Australia has set rules on when to pay CGT but on the flip side, there are some strategies which can help you minimise capital gains tax. In this guide, I will share:

- All you need to know about Capital Gains Tax.

- 3 Important Strategies for Reducing Your Capital Gains Tax on Investment.

- Is it possible to avoid CGT altogether?.

What is Capital Gains Tax?

Capital Gains Tax (CGT) is a tax imposed on the profit made from selling certain assets, such as investment properties, stocks, or businesses. When you sell an asset for more than you paid for it, the difference between the sale price and the purchase price is considered a capital gain.

The capital gain is calculated as the difference between the selling price of the asset and its original purchase price, adjusted for any associated costs like brokerage fees, legal fees, and stamp duty.

When Do You Pay CGT?

You pay CGT when you sell an asset that has increased in value since you acquired it. This tax is triggered by what’s known as a capital gains tax event, which typically occurs when you dispose of an asset, such as selling an investment property or transferring ownership.

CGT is triggered by certain events, such as selling an investment property, transferring ownership of assets, or disposing of shares or businesses.

For Example:

If you purchased a rental property after September 20, 1985, and later decide to sell it for a profit, you would likely be subject to CGT on the capital gain you made from the sale.

3 Strategies to Avoid or Partially Minimize Capital Gain Tax

#1 Main Residence Exemption:

If the investment property has been your main residence, or primary place of residence (PPOR), for a period of time, you may be eligible for a full or partial exemption from CGT.

The property must qualify as your main residence, meeting criteria such as being occupied by you and your family, storing personal belongings there, having utility services connected, and being the address registered on the electoral roll.

You must have lived in the property as your main residence for the entire period of ownership.

The property must not have been used to produce assessable income during your ownership period, meaning it hasn’t been rented out or used for business purposes.

The land on which the property sits should be 2 hectares or less in size.

For Example:

Sarah purchased a property in Sydney in 2010 and lived in it as her primary residence until 2015. In 2015, she decided to move overseas for work and rented out her property. After five years of renting it out, Sarah returned to Sydney and decided to sell her property in 2021.

Since Sarah lived in the property as her main residence for the entire ownership period and met all the eligibility criteria, she was able to claim the main residence exemption on the capital gains from the sale. As a result, Sarah was exempt from paying CGT on the sale of her investment property.

#2 The 6-Year Rule:

This rule allows you to continue treating a property as your main residence for CGT purposes for up to six years after you move out and rent it out. By doing so, you can potentially qualify for the main residence exemption even if you’ve been renting out the property for a period.

This can significantly reduce or eliminate your CGT liability upon the sale of the property. You must have lived in the property as your main residence before renting it out.

The property can be treated as your main residence for CGT purposes for up to six years after you move out and rent it out. During the rental period, you can’t treat any other property as your main residence.

The property should not have been used to produce assessable income during the rental period, except for brief periods while you’re moving between homes. Check out our full guide to Capital gain tax on Investment Property.

For Example:

Mark purchased a property in Melbourne in 2012 and lived in it as his primary residence until 2017. In 2017, Mark was offered a job opportunity in another city and decided to move, renting out his Melbourne property. After three years of renting it out, Mark realized he wanted to sell the property to invest in a new business venture.

Since Mark had lived in the property as his main residence before renting it out, and he sold it within the six-year period, he was able to apply the CGT 6-Year Rule. As a result, Mark was exempt from paying CGT on the capital gains from the sale of his investment property.

#3 Self-Managed Super Fund (SMSF) Investments 12 Months Rule:

Investing in property through a Self-Managed Super Fund (SMSF) can also be a tax-efficient strategy. SMSFs offer tax benefits, such as lower tax rates on rental income and potential CGT discounts. The SMSF can borrow money to purchase the property, allowing it to be used as an investment asset. The rental income from the property within the SMSF is subject to concessional tax rates, with a maximum of 15%.

For instance, if you hold the property in your SMSF for more than 12 months, the tax rate drops from 15% to 10%, and you may be eligible for a CGT discount of up to 33% upon selling the property. Additionally, when the SMSF enters its pension phase, CGT on the sale of the investment property may be entirely exempt.

For Example:

John and Lisa, a married couple, decided to invest in property through a Self-Managed Super Fund (SMSF). They purchased an investment property in Brisbane through their SMSF in 2018. Over the years, the property appreciated in value, and in 2023, they decided to sell it to diversify their investment portfolio.

Since the property was held within their SMSF for more than 12 months, they were eligible for a reduced CGT rate of 10% upon selling the property. Additionally, because they were in the pension phase of their SMSF, they were entirely exempt from paying CGT on the sale of their investment property.

If You Can’t Avoid CGT, Here is How You Can Minimize It

If you’re stuck with Capital Gains Tax (CGT) but want to trim it down, you’ve got options. Even if your property doesn’t get a full exemption, the ATO has ways to shave off your CGT bill when you sell your investment property.

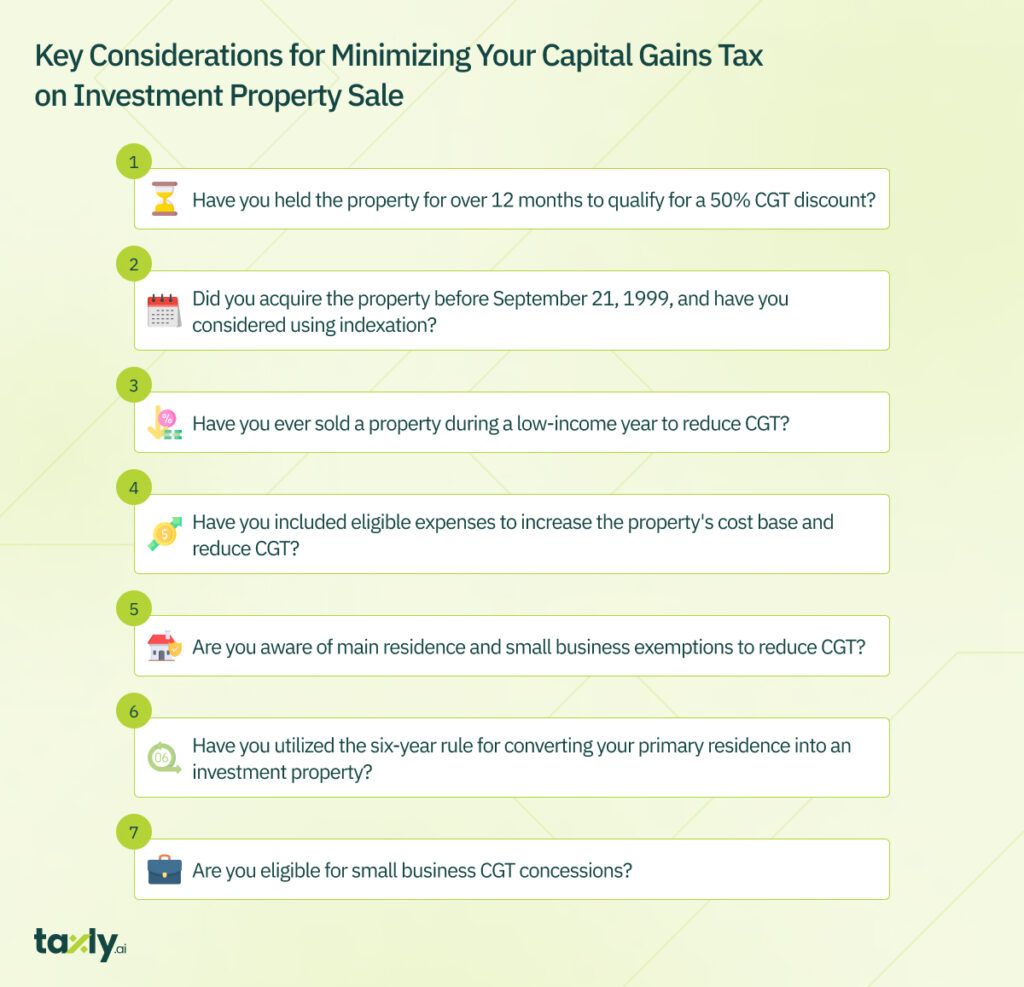

One trick is to boost your cost base by including allowable expenses. These expenses help reduce the capital gains tax you owe.

Here’s how it works: Subtract your cost base from the selling price to figure out your net capital gain. Your cost base is the purchase price plus eligible expenses, minus grants and depreciation.

Eligible expenses cover things like rental advertisement fees, legal costs, stamp duty, and ownership expenses incurred during property searches and inspections.

Plus, expenses for titles, such as legal fees for title organization and defense, and improvements like flooring replacement or deck installation, can be included.

Common expenses that can be included to increase your cost base and potentially reduce your Capital Gains Tax (CGT) liability when selling an investment property:

- Incidental Costs:

- Rental advertisement fees.

- Legal fees related to the sale transaction.

- Stamp duty paid on the purchase of the property.

- Ownership Costs:

- Expenses incurred during property search and inspection, such as travel costs.

- Costs associated with maintaining and managing the property, like property management fees.

- Insurance premiums paid for the property.

- Title Costs:

- Legal fees for the title organization and defense.

- Costs related to transferring the title.

- Improvement Costs:

- Expenses for renovations or repairs done to the property to increase its value.

- Costs incurred for adding extensions or improvements to the property, such as installing a new kitchen or bathroom.

- Expenses for landscaping or outdoor improvements, like installing a deck or patio.

- Professional Services:

- Fees paid to accountants, lawyers, or quantity surveyors for advice or assistance related to the property sale and CGT calculation.

- Valuation fees paid to assess the property’s worth at various stages.

- Finance Costs:

- Loan application fees paid when obtaining financing for the property purchase.

- Interest expenses incurred on loans used to finance the property acquisition or improvements.

Increasing your cost base with these expenses can help you cut down on the chunk of capital gains subject to income tax.

It’s wise to get a quantity surveyor on board to draft a Capital Gains Report. They’ll help identify eligible expenses, optimize your cost base, and crunch the numbers on your capital gains tax liability. This hands-on approach ensures a thorough evaluation and smart handling of your CGT dues.

For Example:

Let’s say you sold your investment property for $500,000. Your purchase price was $400,000. After including eligible expenses of $20,000, your cost base becomes $420,000. Subtracting this from the selling price leaves you with a net capital gain of $80,000, significantly reducing your CGT liability.

Additional Tips to Minimize Your CGT

Wait until You’ve Owned the Property for a Year Before Selling it

It’s a smart move to hold onto your property for over 12 months. Why? Because it can significantly cut down your Capital Gains Tax (CGT) bill. We’ve already talked about the 50% discount that applies to properties held for this duration.

The ke is property indexation, which is a bit more complex. It kicks in only if you bought the property before September 21, 1999. Indexation allows you to adjust the property’s original cost to match its current value, which can help reduce your CGT liability.

Sell When Your Income Takes a Dip

If you foresee a decrease in your income in the coming financial year, consider holding off on the property sale until then. Why? Because it can help lower both your marginal tax rate and your CGT. It’s a strategic move to maximize your savings and minimize your tax burden.

Common FAQs About CGT

How long do you have to live in a house to avoid capital gains tax in Australia?

To avoid CGT, you must reside in a property for at least twelve months for it to be considered your main residence before converting it into an investment property.

Can I invest in another property to avoid capital gains?

No, there is no mechanism to defer CGT by rolling it over to another investment property.

Do retirees pay capital gains tax in Australia?

Yes, unless a retiree qualifies for an exemption, they are still liable to pay CGT.

Who is exempt from paying capital gains tax?

Exemptions from CGT on investment properties apply if:

- You acquired your home before 20 September 1985

- Your property is your primary residence

- You have an eligible granny flat arrangement

Key Takeaways

- CGT is a tax on the profit from selling capital assets like investment properties. It’s calculated based on the difference between the selling price and the purchase price.

- Primary Residence Exemption: No CGT on the sale of your primary home if you meet residency and ownership criteria.

- 6-Year Rule: You can treat your former primary residence as exempt from CGT for up to six years if rented out.

- Small Business CGT Concessions: Small business owners may qualify for CGT discounts and exemptions.

- Increase Cost Base: Include eligible expenses to boost the property’s cost base and reduce taxable gains.

- Hold Assets for Longer: Qualify for a 50% CGT discount by holding assets for over 12 months.

- Strategic Timing: Consider selling assets during low-income years and spreading gains over multiple tax years.

Easily Minimize Your CGT Using Taxly.Ai!

Easily minimize your Capital Gains Tax (CGT) hassle-free with Taxly.Ai, your automated tax assistant. Say goodbye to complex calculations and hello to smarter tax strategies. Sign up now to streamline your CGT process and maximize your savings effortlessly.

Reading List

- Investment Property Tax Deductions in Australia Explained

- How to Lodge Tax Return in Australia?

- Unlocking the Mysteries of Superannuation: Your Comprehensive Guide to Retirement Savings

Comments are closed