We know that financial freedom is at the top of your retirement list and you must be saving your hard-earned money to secure your future. However, it gets overwhelming to track your applicable contribution taxes. In this updated guide, we will reveal effective strategies on how to avoid contribution tax.

We will also break down:

- Latest ATO contribution tax rates and thresholds

- Work from-home Strategies to avoid contribution tax

- Bring forward the rule and its benefits for your savings

- Common pitfalls and tips to avoid penalties

Before talking about the strategies, let’s cover the ATO Contribution tax ground rules:

What is Super Contribution Tax?

Contribution tax is a tax that applies to certain contributions made to your retirement savings account, known as superannuation, in Australia. It’s like a savings plan for your retirement, but there are rules and limits around how much you can contribute without getting taxed.

Two Main Types of Super Contributions Subject to Tax

There are two main types of contributions that may be taxed:

Concessional Contributions:

These are contributions made before tax, like money from your employer, salary sacrifice amounts, or personal contributions you claim as a tax deduction. They get taxed at 15%.

Non-Concessional Contributions:

These are contributions made after you’ve already paid income tax on the money. Usually, they don’t get taxed further.

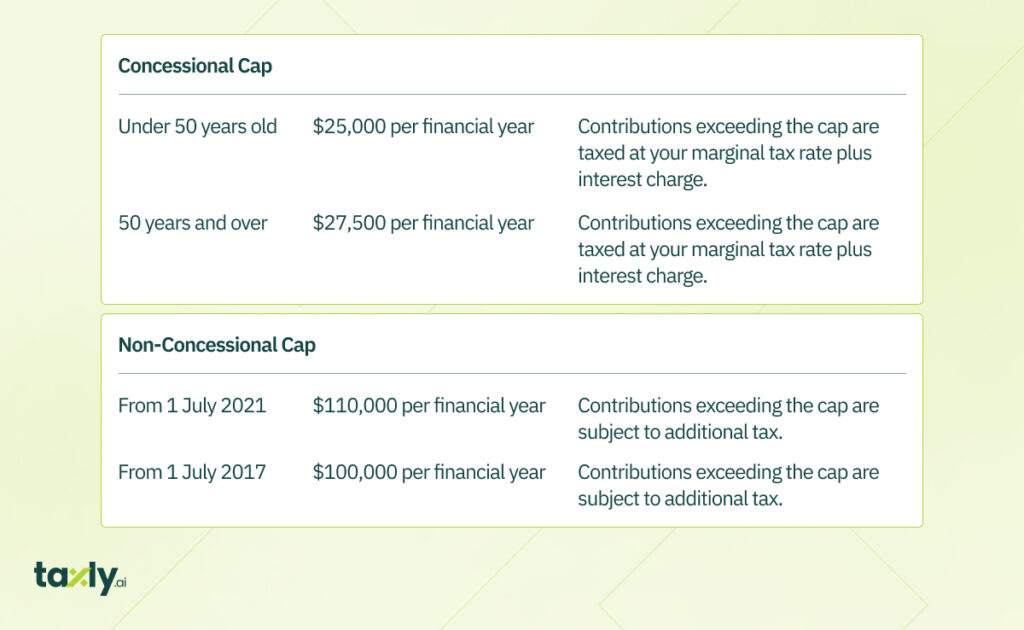

ATO Tax Rates and Thresholds for Super Contribution Tax [UPDATED]

![ATO Tax Rates and Thresholds for Super Contribution Tax [UPDATED]](https://taxly.ai/wp-content/uploads/2023/08/image-1024x597.jpeg)

Concessional Contributions Tax Rate:

If your total concessional contributions exceed the yearly cap (around $25,000 for most people in 2021/2022), the extra amount will be taxed at your normal tax rate, plus an interest charge.

Non-Concessional Contributions Cap:

The cap for non-concessional contributions was $100,000 from 1st July 2017 to 30th June 2021. From 1st July 2021, it increased to $110,000 due to indexation in line with average weekly ordinary time earnings (AWOTE). Your specific cap might be different:

- It could be higher if you can use the bring-forward arrangements.

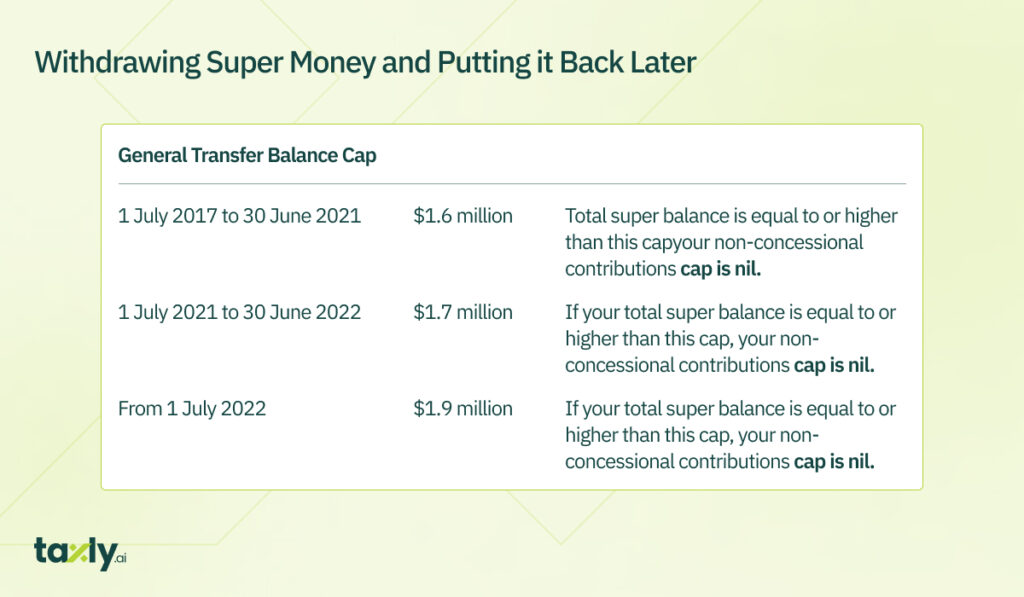

- It might be nil if your total super balance is equal to or greater than the general transfer balance cap, which was $1.6 million from 2017–21 to 2020–21, $1.7 million from 2021–22 to 2022–23, and $1.9 million from 2023–24.

Withdrawing Super Money and Putting it Back Later

If you withdraw money from your super and put it back later, it will count as a new non-concessional contribution, unless you have claimed and been allowed this amount as a tax deduction.

If you have more than one super fund, the total of all non-concessional contributions made to all your funds during a financial year count towards your non-concessional contributions cap.

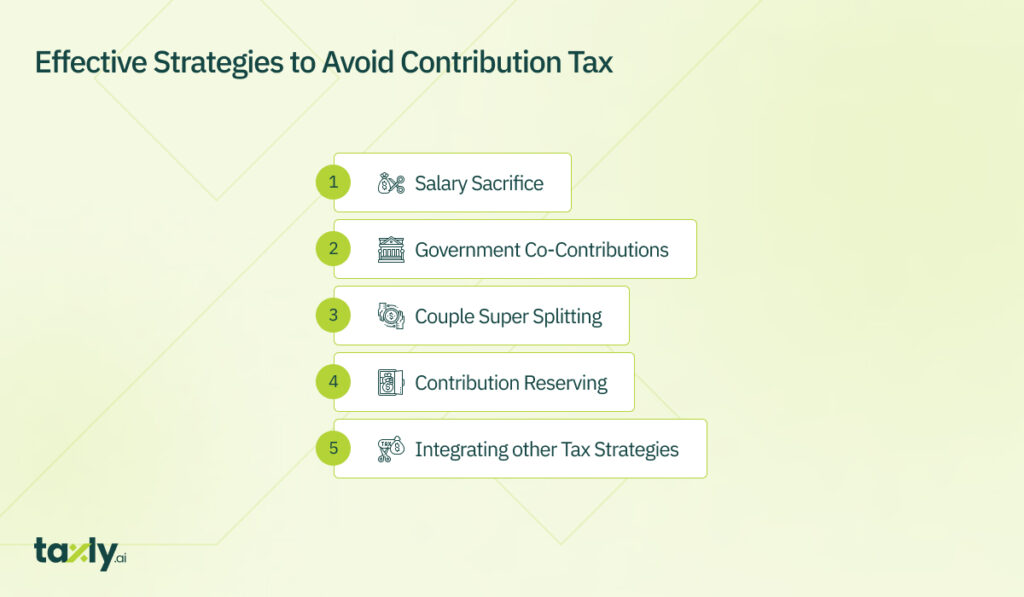

Effective Strategies to Avoid Contribution Tax

Now that you know the basics, let’s talk about ways to avoid contribution tax:

Strategy 1: Salary Sacrifice – Reduce Your Tax!

One effective way to lower contribution tax is through “salary sacrifice.”

You can arrange with your employer to contribute a portion of your pre-tax salary into your superannuation account. This reduces your taxable income, resulting in lower income tax payments.

Keep in mind that salary sacrifice means less take-home pay, as the money is preserved until retirement. Also, consider potential impacts on government benefits tied to your taxable income.

Strategy 2: Government Co-contributions – Get Some Extra Cash!

The government offers a co-contribution scheme to help you save for retirement. If you’re eligible and make personal after-tax contributions to your super, the government will match a portion of it, giving you additional funds for your retirement savings.

To maximize the co-contribution, ensure you meet the eligibility criteria, contribute at least $1,000, and complete your tax return.

For couples, super splitting can be beneficial. It allows you to transfer some of your concessional contributions to your spouse’s super account. This can help equalize retirement savings and potentially reduce contribution tax.

Ensure you meet the eligibility requirements, such as being married or in a de facto relationship, and that your partner is eligible to receive contributions.

Strategy 4: Contribution Reserving – Plan for the Future

Contribution reserving is a strategic move. It involves making concessional contributions in advance to use unused contribution caps later. This approach offers more flexibility and potential tax benefits.

To use contribution reserving, check if your super fund allows it and comply with the relevant conditions.

Strategy 5: Coordinating Contributions with Other Tax Strategies

Coordinate your concessional and non-concessional contributions with other tax-saving strategies to optimize your overall tax position.

Align your contribution tactics with deductions and offsets to minimize your overall tax burden effectively.

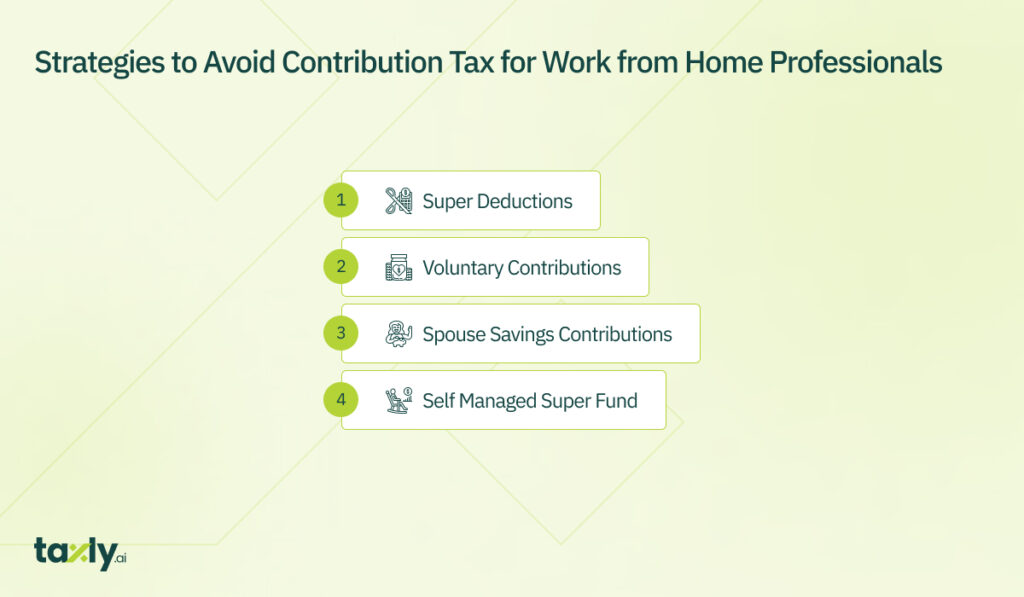

Strategies to Avoid Contribution Tax for Work from Home Professionals

Strategy 1: Get Some Tax Relief with Super Deductions!

When you contribute to your super, you can claim a tax deduction for those personal contributions. It’s like getting a break from your taxes while building up your retirement savings. Cool, right?

Strategy 2: Sign Up for Voluntary Contributions!

You’re in the driver’s seat! Consider making extra contributions to your super on top of what your employer puts in. You’ve got options – you can go with before-tax (concessional) or after-tax (non-concessional) contributions.

Concessional contributions give you instant tax benefits, while non-concessional ones grow tax-free in your super. So, you decide how much and when, giving your retirement savings an extra boost while managing your tax smartly.

Suggested Read: Work from Home Tax Deduction In Australia: Check Your Eligibility

Hey, lovebirds! If your spouse earns less than $40,000, you can lend a helping hand to their super and score some tax benefits for yourself. It’s a win-win situation!

When you contribute to your spouse’s super, you could be eligible for a tax offset of up to $540 per year—less tax for you, and more super for your loved one.

Strategy 4: Start a Self-Managed Super Fund (SMSF)

Ready to be the boss? Consider setting up a Self-Managed Super Fund (SMSF) if you’ve got a substantial super balance and want more control over your investments and tax strategies.

With an SMSF, you can choose where your money goes and make investment decisions that match your financial goals. Plus, it opens doors to savvy tax moves and flexibility in managing your super. Pretty cool, right?

If You Are Stuck, Seek Professional Advice

Consider consulting a qualified tax advisor. They will tailor strategies to your specific situation and help you make informed decisions to maximize your contributions and super savings.

The Bring-Forward Rule – Maximize Your Super Contributions:

Alright, let’s get down to business and talk about the bring-forward rule – a powerful strategy to boost your super contributions and secure a solid retirement plan!

Age and Eligibility:

Here’s the deal:

- If you’re below 65 years old at any time during a financial year, you’re in for a treat! You can make non-concessional contributions up to 3 times the annual cap. That means you can put in three times the usual amount!

- But if you turn 65 before 1st July, the rule won’t apply to you that financial year. No worries, though – you might still contribute if you meet certain conditions.

Maximum Contribution Limit:

The maximum amount you can contribute under the bring-forward rule is 3 times the annual non-concessional cap. So, if the cap is $110,000 – you can contribute up to $330,000 in one go!

Work Test and Work Test Exemption:

If you’re aged 67 to 74, you might need to meet the work test or work test exemption to benefit from this rule. It’s not a biggie – just a small requirement to be eligible for the super party!

Handy Tips:

- Keep an eye on your contributions – don’t go over the cap to avoid unnecessary taxes.

- Timing is crucial! Before making significant contributions, consider your financial situation.

- Stay updated! Changes to caps or eligibility can happen, so stay informed.

What Happens if you Exceed the Cap?

If you exceed your non-concessional contributions cap, the Australian Taxation Office (ATO) will notify you, and you may have to pay extra tax. Additionally, you will be required to lodge a tax return for that year.

Remember, tax rules might change, so it’s a good idea to check with the ATO or talk to a tax expert to stay up-to-date and avoid any surprises.

Tips to Avoid Exceeding the Non-Concessional Contributions Cap

Keep track of your contributions: Monitor your contributions throughout the year to ensure they stay within the non-concessional cap.

Review your super balance: Consider checking your super balance before making any non-concessional contributions to ensure you won’t exceed the cap.

Seek professional advice: If you’re unsure about the rules or how much you can contribute, consult a tax expert to avoid any potential tax issues.

The Bottomline

Saving up for the future is your right and responsibility. Contribution taxes affect your saving potential and impact your future situation. ATO urges you to track your applicable contributions cap and thresholds to avoid any penalties. You can adopt several strategies to avoid contribution tax and maximize your savings. If you feel stuck, seek professional advice.

Related Links:

- How to Lodge Tax Return in Australia?

- Can You Claim Deductions Without Receipts in Australia?

- What is Marginal Tax Rate in AU – [FY 2023-24] Complete Guide

Comments are closed