In Australia, a de facto relationship is defined as a couple living together on a genuine domestic basis in a relationship, without being legally married or in a registered relationship. If you are in a de facto relationship, you must declare your partner on your de-facto tax return.

Tax Obligations for De Facto Couples

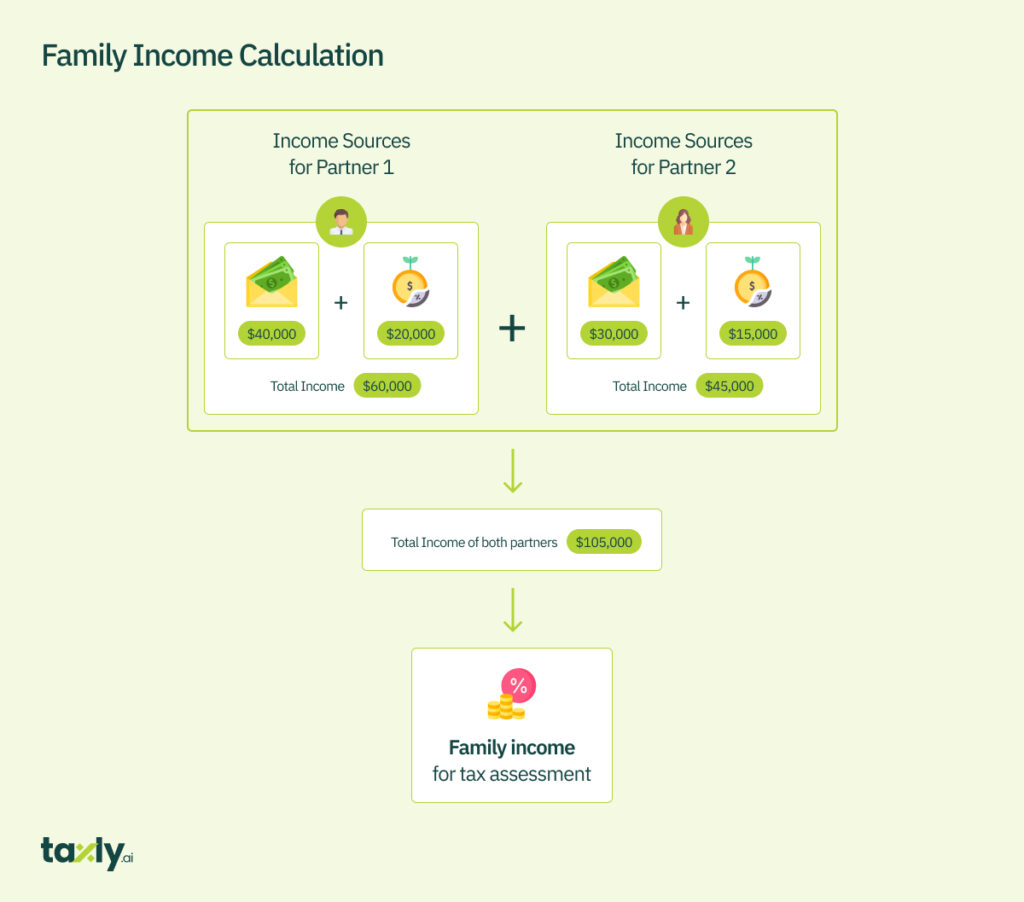

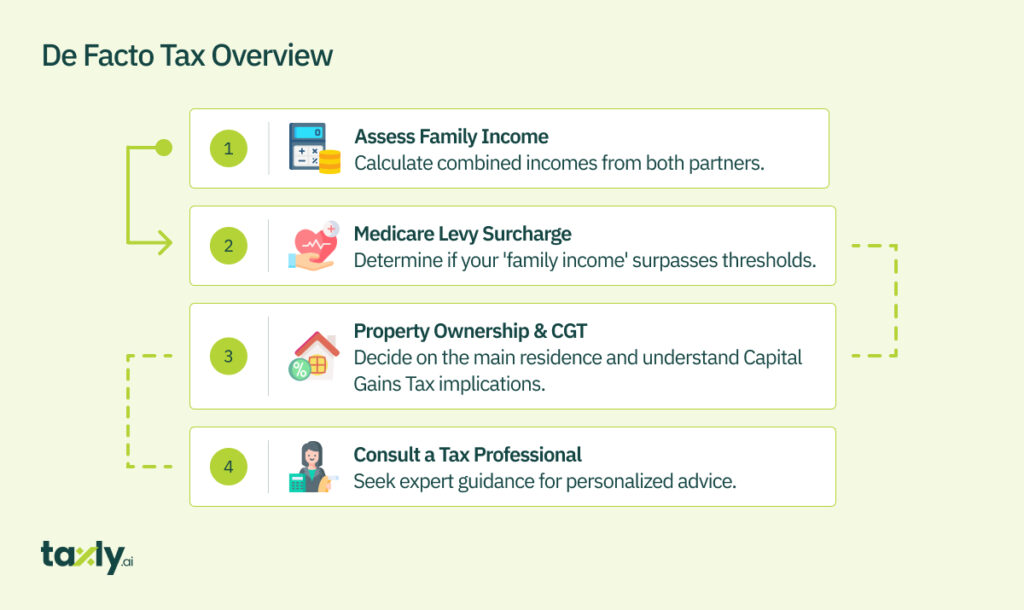

As a de facto couple, your income is assessed jointly and referred to as “family income”

This means that you still lodge a personal tax return each year, but you include your partner’s income on it as well. The Australian Taxation Office (ATO) uses your joint income to calculate tax offsets you may be entitled to receive.

Partner’s Financial Details Required for De-Facto Tax

You’ll need to report various financial details about your partner, such as:

- Taxable Income

- Trust Distributions

- Reportable Fringe Benefits

- Pensions and Allowances

- Reportable Super Contributions

- Foreign Income

For instance, let’s say your partner earns $50,000 in taxable income and receives a $5,000 pension. These figures are included in your ‘family income’ calculation.

Implications of De Facto Tax Changes

Tax changes in a de facto relationship can have both positive and negative impacts:

Medicare Levy Surcharge:

If your ‘family income’ crosses the Medicare Levy Surcharge threshold, you may need to pay the surcharge. For instance, if your income is $190,000 and your partner’s is $20,000, the combined ‘family income’ triggers the surcharge [1].

Private Health Cover Rebate:

If your family income falls within a specific range and you have private health cover, you may be eligible for a rebate, which can be applied as a premium discount or claimed on your tax return.

Tax Refund:

Conversely, if your ‘family income’ remains below certain limits, you may receive a higher tax refund. Consider this example: if your joint income is $150,000, you might benefit from a larger refund.

Suggested Read: How to Lodge Tax Return in Australia?

De-Facto Tax and Property Ownership

If both partners own properties, you need to consider Capital Gains Tax (CGT). CGT is a levy on the increase in property value between purchase and sale dates.

Determine your Main Residence:

Decide which property serves as the main residence, eligible for CGT exemptions. For instance, if both partners own homes, you can choose one as the primary residence for tax purposes.

De-Facto Tax CGT Exemption Requirements:

To be eligible for a CGT exemption, the property should meet specific criteria.

- It must have been your primary residence during the ownership period

- It must not used for income generation

- It should be situated on less than two hectares of land.

Gender and De Facto Relationships

It’s worth noting that the ATO does not care about sex or gender when it comes to defining a spouse or de facto partner. The gender of your partner, and your gender, has nothing to do with the definition of a spouse or de facto partner for tax purposes.

History of De Facto Tax in Australia

The history of Australia’s tax system dates back to the Second World War when fundamental changes were made to the taxation system.

Income taxation was consolidated by the federal government in 1942.

At the time of Federation, Australia’s tax to GDP ratio was around 5%, and this ratio remained reasonably constant until the introduction of the federal income tax in 1915, which was used to fund Australia’s war effort.

Tax revenues tended to fall in the middle of the twentieth century, and by 1963-64, the tax take was around 18% of GDP.

It then increased significantly between 1973 and 1975, largely as a result of increased funding for social programs [2]

There has since been a modest rise in Australia’s tax take, similar to the experience of many other OECD countries.

When declaring for de facto, you will need to answer the following questions:

- What is your spouse’s name, date of birth, and gender?

- What is your relationship status (married or de facto)?

- If you were not in a de facto relationship for a full year, what were the commencement and/or end date within the current financial year?

- What is your spouse’s income?

- What is the amount of Australian Government pensions and allowances that your spouse received, including tax-free and exempt payments?

- What are your spouse’s reportable superannuation contributions (including both reportable employer superannuation contributions and deductible personal superannuation contributions)?

- What is your spouse’s total reportable fringe benefits amounts (including both exempt and non-exempt amounts)?

The Bottomline

De facto tax in Australia is applicable on de facto relationships. You must declare your partner on your tax return, and your income is assessed jointly as “family income”. The Australian Taxation Office (ATO) uses your joint income to calculate tax offsets you may be entitled to receive.

Discover More Topics

- Australian Goods and Service Tax [EXPLAINED]

- How to Avoid Contribution Tax – ATO Tax Threshold [Updated 2023-24]

- Sole Trader Tax Deductions in Australia: A Comprehensive Guide

References:

[1] Australia Tax Summaries – PWC

[2] Australia Tax History – Treasury AU