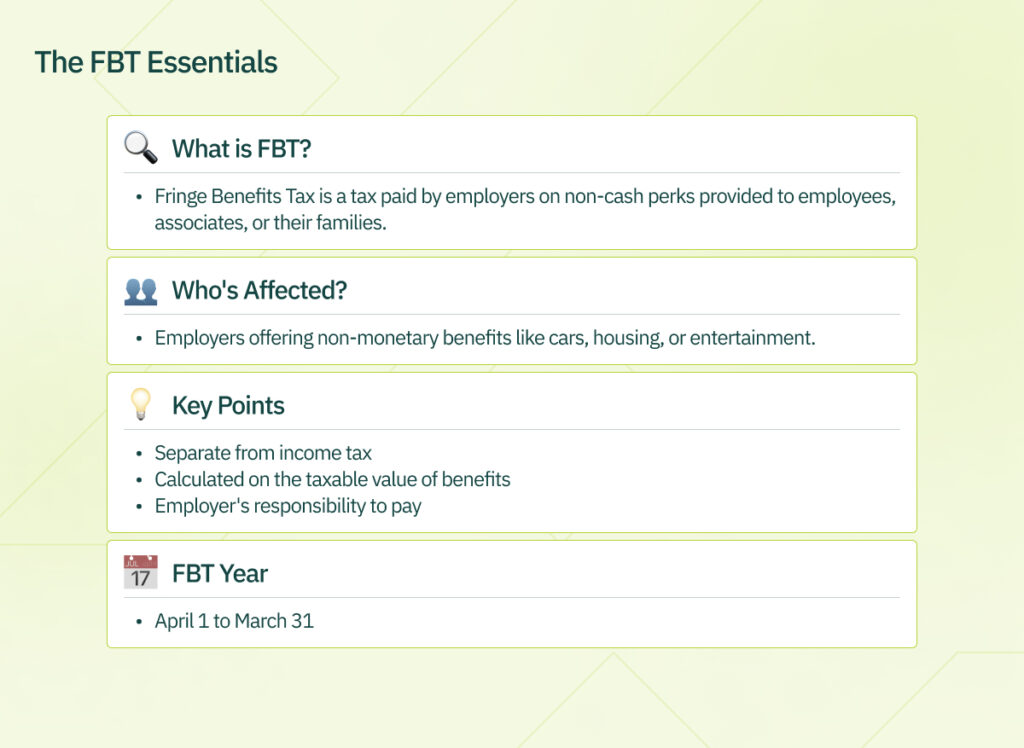

Fringe Benefits Tax (FBT) in Australia is a tax imposed on employers for the various benefits they provide to their employees, as well as the employees’ family or associates. Unlike income tax, FBT is the responsibility of the employer and is calculated based on the taxable value of the fringe benefit.

Fringe Benefits Tax Australia – Key Takeaways

- The FBT year runs from April 1 to March 31.

The FBT rate is currently 47%. The Type 1 gross-up rate is 2.0802 and the Type 2 gross-up rate is 1.8868 (Source: ATO FBT Rate). - If an employer’s FBT liability for the last year was $3,000 or more, they will need to pay 4 quarterly installments.

- Reportable fringe benefits must be included on employees’ payment summary or Single Touch Payroll (STP) income statement if the benefit exceeds $2,000.

- Minor benefits (less than $300 in value) incurred infrequently and irregularly are exempt from FBT.

- Remote area housing, living away from home allowances (partly exempt), employee relocation expenses, superannuation (retirement/private pension contributions), protective clothing, tools of trade, briefcases, and mobile phones are exempt from FBT.

- Expats working in Australia may be subject to FBT if they receive benefits such as housing, car allowances, or other non-cash perks from their employer.

Are you Eligible for Any FBT Deductions or GST Credits?

Employers in Australia are eligible to claim an income tax deduction and GST credits for the cost of providing fringe benefits, provided they are eligible to claim GST credits.

However, to be eligible to claim GST credits, the benefits must be incurred for the purpose of the business and must not be a non-claimable item listed under Regulations 26 and 27 of the GST (General) Regulations, or given only to the Sole Proprietor, Partners, or Directors of the company.

Eligible FBT Deductions:

Business-Related Expenses:

Businesses can deduct the costs associated with providing fringe benefits. For instance, if you organize work-related training sessions for employees, the expenses can be claimed as FBT deductions.

Example: Hosting a professional development workshop for your team.

Suggested Read: Your Complete Guide to Work Related Business Trip Tax Deduction

De Minimis Benefits:

Small, infrequent benefits, known as de minimis, may not attract FBT. This could include minor benefits like morning teas or small birthday gifts.

Example: Organizing a modest office celebration for a colleague’s birthday.

Portable Electronic Devices:

Providing portable electronic devices like laptops or smartphones to employees can be considered an eligible deduction for FBT.

Example: Supplying company smartphones for work purposes.

GST Credits for FBT:

GST-Registered Businesses:

GST-registered businesses can claim GST credits for expenses related to fringe benefits. This provides a means to offset some of the costs associated with providing these benefits.

Example: Catering costs for a business event where employees receive fringe benefits.

Business-Use Assets:

If a fringe benefit involves assets that are used for both business and personal purposes, businesses may be eligible for GST credits on the business-use portion.

Example: Providing a company car used for work-related travel.

Input-Taxed Supplies:

While some supplies may be input-taxed for GST purposes, businesses may still be eligible for GST credits when it comes to FBT.

Example: Offering discounted gym memberships, which are typically considered input-taxed for GST.

How to Calculate Fringe Taxable Value?

FBT is calculated on the grossed-up value of the fringe benefit. This value includes the actual benefit amount plus the FBT payable, equivalent to the gross income employees would need at the highest marginal tax rate (47%, including the Medicare levy) to purchase the benefit themselves.

What is the current FBT Rate and Liability?

The current FBT rate is 47%. Employers must self-assess their FBT liability for the FBT year, which runs from April 1 to March 31. If they have an FBT liability, they must lodge an FBT return and pay the owed tax.

How to Report Fringe Benefit Tax to ATO?

Businesses providing fringe benefits must register for FBT, calculate the FBT payable, keep comprehensive records of the benefits offered, and lodge a return by May 21.

Reportable fringe benefits should also be included on employees’ payment summaries or Single Touch Payroll (STP) income statements.

The FBT year aligns with the Australian financial year, running from April 1 to March 31 (source: ATO FBT).

Step-by-Step Process:

Assess FBT Liability:

Determine if your business provided fringe benefits during the FBT year (April 1 to March 31).

Register for FBT:

Ensure your business is registered for FBT with the Australian Taxation Office (ATO).

Calculate Taxable Value:

For each fringe benefit, calculate the taxable value, including the actual benefit and FBT payable.

Self-Assess and Lodge FBT Return:

Self-assess your FBT liability, and if applicable, lodge the FBT return by May 21 following the end of the FBT year.

Pay FBT Owed:

Remit any FBT liability to the ATO by the specified due date.

Maintain Records:

Keep detailed records of fringe benefits, calculations, and supporting documents for compliance and potential audits.

Claim Deductions and GST Credits:

If eligible, claim income tax deductions and GST credits for costs related to providing fringe benefits.

Reflect in Employee Records:

Report fringe benefits on employees’ payment summaries or Single Touch Payroll (STP) income statements.

For Example:

If your business provides a company car as a fringe benefit, calculate the taxable value considering the car’s value and the additional amount at the highest marginal tax rate.

What About Expatriates?

Expatriates working in Australia may be subject to FBT if they receive non-cash benefits such as housing or car allowances. The responsibility for paying FBT rests with the employer providing these fringe benefits.

For Example:

If an employee receives a company car as a fringe benefit, the taxable value for FBT purposes would include the value of the car plus the additional amount calculated at the highest marginal tax rate.

Which items are Exempt from Fringe Benefits Tax?

Work Gadgets:

Laptops, tablets, or work phones provided for job tasks are usually exempt from FBT.

Tools of the Trade:

Equipment or tools given for work-related purposes may be exempt.

Small Nice Things:

Benefits valued at $300 or less, provided occasionally, and not part of a salary package, may be exempt.

Health Perks:

Some employer-provided health benefits, like vaccinations, may be exempt.

Moving Help:

Certain benefits for employees relocating for work might be exempt.

Special Vehicles:

Work-related vehicles with limited personal use, like taxis or certain vans, may qualify for exemptions.

Emergency Aid:

Help provided during emergencies, such as accommodation or transport, could be exempt.

Education Support:

Costs for work-related education and training may be exempt in certain cases.

Outback Living:

Housing in remote areas for business needs might be exempt.

Living Away from Home Allowance (LAFHA):

Some LAFHAs for employees living away from home for work reasons may be exempt.

The Bottom Line

Fringe Benefit Tax in Australia is a tax on non-cash benefits provided by employers to employees and associates. Employers must calculate, report, and pay FBT to comply with Australian tax regulations.

Discover More Topics

- Investment Property Tax Deductions in Australia Explained

- What can Childcare Workers Claim on Tax? [Complete Guide]

- 10 Self-Employment Tax Deductions and Benefits for Australians

Comments are closed