Superannuation for a sole trader is your ticket to a secure retirement, a customized savings plan crafted by you, for you. It’s not just about meeting obligations; it’s about seizing opportunities. So, saddle up as we break down what superannuation means for you, what to know, and how to master this crucial aspect of your financial journey.

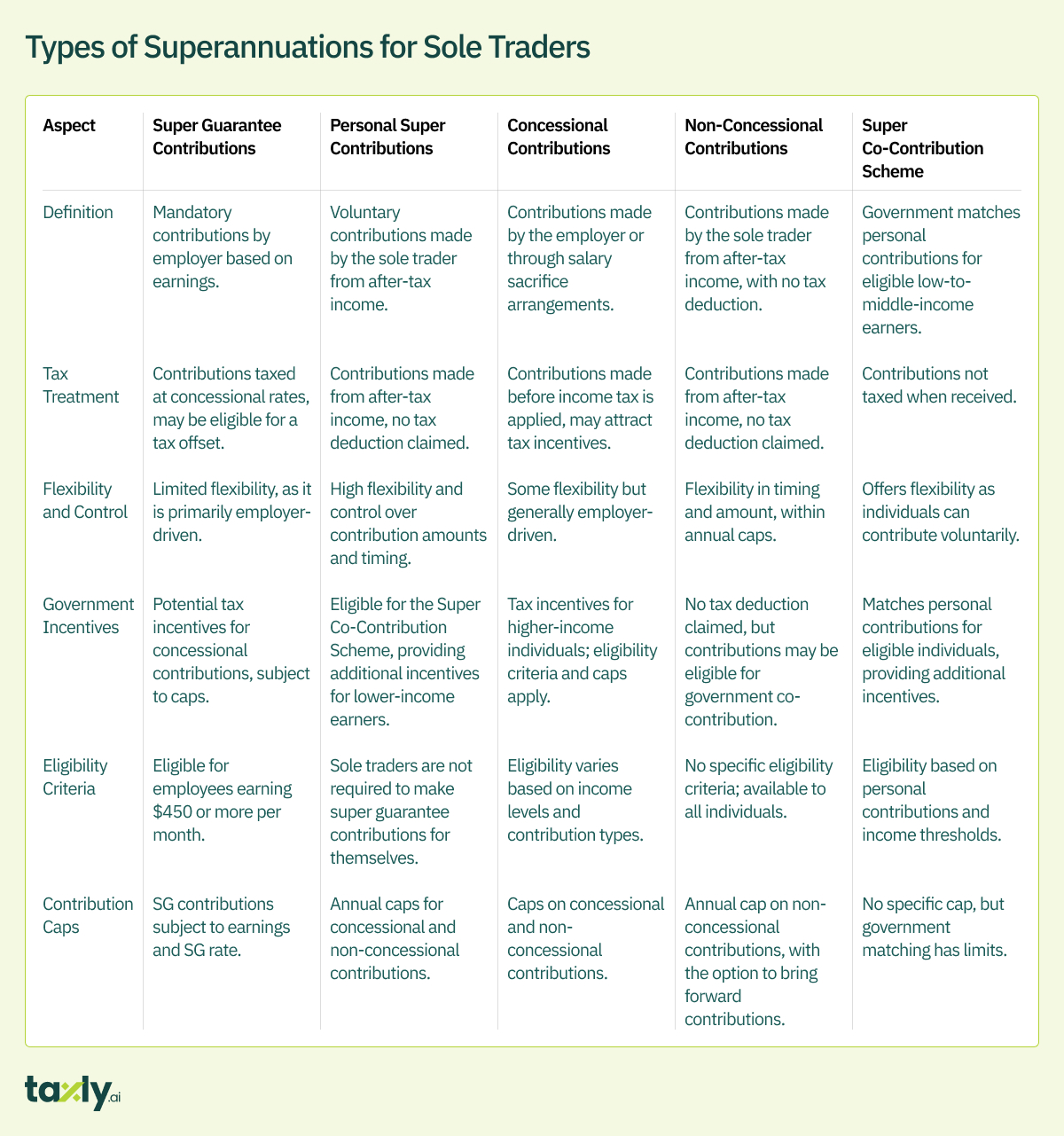

Types of Superannuations for Sole Traders:

Superannuation Guarantee Contributions:

Superannuation Guarantee (SG) contributions are mandatory contributions made by employers on behalf of their eligible employees into their superannuation funds. These contributions are designed to ensure that employees receive a portion of their income as savings for retirement.

- Mandatory: Employers are required by law to make SG contributions on behalf of eligible employees.

- Percentage: As of the 2023/24 financial year, the SG rate is 11% of an employee’s ordinary time earnings.

- Ordinary Time Earnings: Contributions are calculated based on an employee’s ordinary time earnings, excluding overtime.

Eligibility:

Employees are eligible for SG contributions if they are over 18 years old and earn $450 or more (before tax) in a calendar month.

Eligible employees include full-time, part-time, and casual workers.

Calculation of Contributions:

SG contributions are calculated based on the employee’s ordinary time earnings, which include their normal working hours and specific allowances but exclude overtime.

Payment Frequency:

Employers are required to make SG contributions at least quarterly, with specific deadlines for payment.

Cap on Contributions:

There is a cap on the maximum earnings on which SG contributions are calculated. As of the 2023/24 financial year, this cap is $58,920 per quarter.

Contribution Schedule:

The SG rate is set to increase gradually, aiming for 12% by the 2025/26 financial year. This is part of a phased increase to enhance retirement savings for employees.

Employee Choice of Fund:

Employees have the option to choose their superannuation fund, but employers must contribute to the chosen fund.

Penalties for Non-Compliance:

Employers who fail to meet their SG obligations may face penalties and charges. The Australian Taxation Office (ATO) monitors compliance and takes action against non-compliant employers.

Impact on Employees:

SG contributions form a crucial part of employees’ retirement savings, providing a consistent stream of contributions to their superannuation funds.

Employees can track their SG contributions on their payslips and through their superannuation statements.

Considerations for Sole Traders:

Sole traders are not required to make SG contributions for themselves. However, they have the option to make personal super contributions.

Example: If a sole trader earns $100,000, they are not required to contribute a specific percentage of their income to their super fund as mandatory super guarantee contributions.

Personal Super Contributions:

Personal super contributions refer to voluntary contributions that individuals make to their superannuation fund from their after-tax income. Unlike employer contributions or salary sacrifice arrangements, personal contributions are made at the discretion of the individual to enhance their retirement savings.

Key Characteristics:

Voluntary: Individuals choose to make personal contributions to their superannuation fund.

After-Tax Income: Contributions are made from income that has already been taxed at the individual’s marginal tax rate.

Tax File Number (TFN): It is important to ensure the superannuation fund has the individual’s TFN to avoid higher taxes on contributions.

Key Points:

Flexibility:

Personal super contributions offer flexibility as individuals can choose when and how much they contribute to their super fund.

This flexibility allows for additional contributions beyond the mandatory Superannuation Guarantee contributions.

Tax Implications:

Individuals do not claim a tax deduction for personal contributions from after-tax income.

Personal contributions are not subject to the concessional contributions cap.

Contribution Limits:

While there is no cap on the amount of personal contributions, there are caps on concessional (before-tax) and non-concessional (after-tax) contributions.

Monitoring these caps is important to avoid potential penalties.

Tax File Number (TFN):

It is crucial for individuals to provide their TFN to the superannuation fund when making personal contributions to avoid higher tax rates on contributions and to receive the government co-contribution if eligible.

Suggested Read: How do I Find my Tax File Number in Australia?

Super Co-Contribution Scheme:

Individuals making personal contributions may be eligible for the government’s Super Co-Contribution Scheme.

The government matches personal contributions on a sliding scale, providing an additional incentive for individuals in lower income brackets.

Claiming a Tax Deduction:

Individuals who wish to claim a tax deduction for their contributions may choose to make concessional contributions instead.

If a tax deduction is claimed, the contribution is no longer considered a personal contribution for the Super Co-Contribution Scheme.

Suggested Read: Sole Trader Tax Deductions in Australia: A Comprehensive Guide

Impact on Retirement Savings:

Personal super contributions allow individuals to take control of their retirement savings by contributing additional funds beyond mandatory contributions.

The timing and amount of personal contributions can be adjusted based on individual financial circumstances.

Example: A sole trader earning $60,000 annually decides to contribute $5,000 of their income to their super fund, providing an additional savings avenue beyond the mandatory contributions.

Concessional Contributions:

Concessional contributions include before-tax contributions, such as employer contributions and salary sacrifice arrangements. The cap for concessional contributions is $27,500 for the 2023-24 financial year.

Concessional contributions are contributions made to a superannuation fund from pre-tax income. These contributions are generally made through employer contributions or salary sacrifice arrangements, where the individual agrees to forgo part of their salary in exchange for additional super contributions.

Key Characteristics:

- Taxation: Contributions are made before income tax is applied, reducing the individual’s taxable income.

- Source of Funds: Contributions are made with money that has not yet been subjected to income tax.

- Cap: There is an annual cap on concessional contributions, and exceeding this cap may result in additional tax.

Examples:

- Employer contributions, including the Superannuation Guarantee contributions.

- Salary sacrifice contributions, where an employee agrees to sacrifice part of their salary to contribute to super before tax is applied.

Example: A sole trader with a taxable income of $80,000 has $10,000 contributed to their super by their business, ensuring compliance with the $27,500 concessional contributions cap.

Non-Concessional Contributions:

Non-concessional contributions are contributions made to a superannuation fund from after-tax income. These contributions are made with money that has already been taxed at the individual’s marginal tax rate.

Key Characteristics:

- Taxation: No tax deduction is claimed for these contributions.

- Source of Funds: Contributions are made with money that has already been subjected to income tax.

- Cap: There is an annual cap on non-concessional contributions, and exceeding this cap may result in additional tax.

Examples:

- Using personal savings to contribute to super.

- Receiving an inheritance and directing a portion of it to the superannuation fund.

A sole trader with a total super balance of $1.8 million decides to bring forward two years’ worth of non-concessional contributions, contributing $300,000 to their super over three years, staying within the $330,000 cap.

Super Co-Contribution Scheme:

The Super Co-Contribution Scheme is a government initiative designed to encourage low-to-middle-income individuals, including sole traders, to make personal contributions to their superannuation. The government matches these personal contributions with a co-contribution, providing an additional boost to the individual’s retirement savings.

Eligibility Criteria:

- Sole traders are eligible for the scheme if they make personal super contributions from their after-tax income.

- The scheme is particularly beneficial for those with lower incomes, as it aims to provide targeted support.

Government Matching:

When a sole trader makes a personal super contribution, the government matches it up to specified limits.

The matching rate and maximum co-contribution amount vary based on the individual’s income.

Impact on Retirement Savings:

For sole traders, the co-contribution can significantly enhance their retirement savings without requiring additional employer contributions.

It serves as a government incentive to encourage voluntary contributions and promote long-term financial security.

Income Thresholds:

The eligibility and amount of the co-contribution depend on the individual’s total income. There are specific income thresholds that determine the co-contribution amount.

Sole traders should be aware of these thresholds to maximize their benefits under the scheme.

Tax Implications:

The co-contribution is not subject to tax when received. However, sole traders should consider their overall tax situation, as claiming a tax deduction for personal contributions renders them ineligible for the co-contribution.

Example: A sole trader earning $40,000 makes a $500 personal contribution to their super. The government matches this with a $500 co-contribution, effectively doubling their savings.

Low-Income Super Tax Offset (LISTO):

The Low-Income Super Tax Offset (LISTO) is a government initiative aimed at supporting low-income earners, including sole traders, by providing a tax offset on their concessional (before-tax) superannuation contributions. This offset helps to ensure that low-income individuals receive effective tax relief on their super contributions, making it more financially viable for them to save for retirement.

Targeted Tax Relief:

LISTO provides tax relief specifically for individuals with low incomes who make concessional super contributions.

Sole traders with taxable incomes within the eligible range can benefit from this offset.

Eligibility Criteria:

Sole traders are eligible for LISTO if their adjusted taxable income is less than $37,000.

Adjusted taxable income includes assessable income, reportable fringe benefits, and certain other amounts, minus any allowable deductions.

Calculating the Offset:

The LISTO is calculated as 15% of the concessional super contributions made during the financial year, up to a maximum offset of $500.

Sole traders should be aware of the cap on concessional contributions to maximize the offset effectively.

Automatically Applied:

The LISTO is generally automatically applied by the Australian Taxation Office (ATO) based on the information provided by super funds and individual tax returns.

Sole traders don’t need to separately apply for the LISTO.

Impact on Low-Income Sole Traders:

LISTO effectively reduces the tax paid on concessional super contributions for low-income sole traders.

This can make contributing to super more attractive and financially beneficial, particularly for those with modest incomes.

Taxable Income Considerations:

Sole traders should consider their overall taxable income, including any income from their business, to determine eligibility for LISTO.

The offset helps ensure that a portion of the tax paid on super contributions is returned to low-income earners.

Example: A part-time sole trader earning $25,000 benefits from the LISTO, receiving a tax offset on their $2,000 concessional contributions.

Spouse Contributions:

Spouse contributions refer to the practice where one spouse contributes money to the superannuation account of their spouse. This contribution is a way to boost the retirement savings of the receiving spouse, especially when they may have lower income or are not currently working. It’s a strategy aimed at strengthening the financial well-being of both spouses in retirement.

How do Spouse Contributions Work?

Contributor and Recipient:

The contributing spouse is the one making the contribution to their partner’s superannuation account.

The receiving spouse is the one whose superannuation account receives the contribution.

Eligibility:

To be eligible for spouse contributions, the receiving spouse must be under the age of 75.

The contributing spouse must also meet certain income and work tests.

Tax Offset:

The contributing spouse may be eligible for a tax offset based on the amount contributed to their partner’s super.

The offset is subject to specific conditions and is designed to provide financial support to couples managing their retirement savings.

Example: A sole trader’s spouse contributes $3,000 to their super, qualifying for a tax offset based on their partner’s income.

Downsizer Contributions:

Downsizer contributions are a special type of contribution to superannuation in Australia that allows individuals aged 65 and older to contribute proceeds from the sale of their home into their superannuation fund. This initiative aims to provide older Australians with an additional option for managing their finances as they transition to retirement.

How do Downsizer Contributions Work?

Eligibility:

To be eligible for downsizer contributions, the individual must be 65 years or older at the time of making the contribution.

The home sold must have been owned for a specific period.

Contribution Limits:

Downsizer contributions are capped at $300,000 per individual or $600,000 per couple.

These contributions are in addition to the existing contribution caps and are not subject to age-based restrictions.

Property Sale Requirements:

The property sold must have been the individual’s main residence at some point.

There is no requirement for the individual to purchase a new home after selling their current residence.

Suggested Read: Investment Property Tax Deductions in Australia Explained

Timing of Contribution:

Downsizer contributions must be made within 90 days of receiving the proceeds from the sale.

Extensions may be granted in specific circumstances, but it’s essential to adhere to the timeframes.

Tax Implications:

Downsizer contributions are exempt from the age-based work test and restrictions that typically apply to contributions from individuals aged 67 to 74.

These contributions are not subject to capital gains tax (CGT).

Effect on Total Super Balance:

Downsizer contributions do not count towards the individual’s total super balance, which can be advantageous for those close to the total super balance cap.

Financial Planning Considerations:

Individuals considering downsizer contributions should assess their overall financial situation and goals.

Seeking advice from a financial planner or tax professional is advisable to optimize the benefits and navigate potential implications.

One-Time Opportunity:

Downsizer contributions are a one-time opportunity for each individual. Once the contribution is made, they cannot make additional downsizer contributions in the future.

Example: A retiree sells their property and contributes $300,000 to their super under the downsizer contributions scheme.

Superannuation for a Sole Trader – FAQs

Does sole trader need to pay superannuation?

No, sole traders are not obligated to pay superannuation for themselves. It’s optional, and they can make voluntary contributions to boost their retirement savings.

Do ABN holders get superannuation?

ABN holders, including sole traders, are not entitled to receive superannuation guarantee contributions from an employer. They can make personal contributions if desired.

What is the $450 super threshold?

The $450 super threshold is the minimum monthly income an employee must earn from a single employer to be eligible for superannuation guarantee contributions. Amounts below this threshold may not trigger super contributions.

Is it worth claiming a tax deduction on super contributions?

It depends on individual circumstances. Claiming a tax deduction for super contributions can reduce taxable income, but it may impact eligibility for certain government benefits. It’s advisable to assess the overall financial situation before making this decision.

The Bottomline

As a sole trader, your superannuation is more than a mandatory savings account – it’s a personalized financial toolkit for your retirement. Keep a watchful eye on contribution caps, stay flexible in your approach, and view superannuation not just as an obligation but as a strategic opportunity to craft a retirement that aligns with your unique goals. Ultimately, it’s about taking control of your financial destiny, making informed choices, and ensuring that your superannuation becomes a powerful asset in your journey towards a secure and fulfilling retirement.

Discover More Topics

- Unlocking the Mysteries of Superannuation: Your Comprehensive Guide to Retirement Savings

- Australian Goods and Service Tax [EXPLAINED]

- 10 Self-Employment Tax Deductions and Benefits for Australians

Comments are closed